- 8 MIN READ

- Views: 492

How to build a Fintech App with AI in 2026

By Ram Nethaji

Founder

AI Fintech App Development

AI-Powered Finance Solutions

AI-Based Payment App Development

A few years ago, building a fintech app meant hiring a full team, spending months on development, and investing a serious budget before you even saw a working product.

In 2026, AI tools can help you sketch screens, write chunks of code, and even connect basic features without starting from scratch. For someone with an idea, it feels like the barrier to entry has dropped. You can move faster, test quicker, and get something functional in front of users without waiting forever.

But fintech isn’t just about getting an app to work.

The moment real money, user data, and transactions come into the picture, things get heavier. There are regulations to follow, systems that can’t afford to fail, and security standards that go far beyond what most AI-generated setups can handle on their own.

So while AI has made building easier, it hasn’t made fintech simple.

In this blog, we’ll look at how far AI can actually take you when building a fintech app, and where things start to demand a more structured, expert approach.

What is a fintech app?

A fintech app is a mobile or web application that helps people manage, move, or grow their money using digital technology.

In simple terms, if an app lets you handle financial tasks without going to a bank or dealing with paperwork, it falls under fintech. Fintech apps are built to make financial services faster, more accessible, and easier to use.

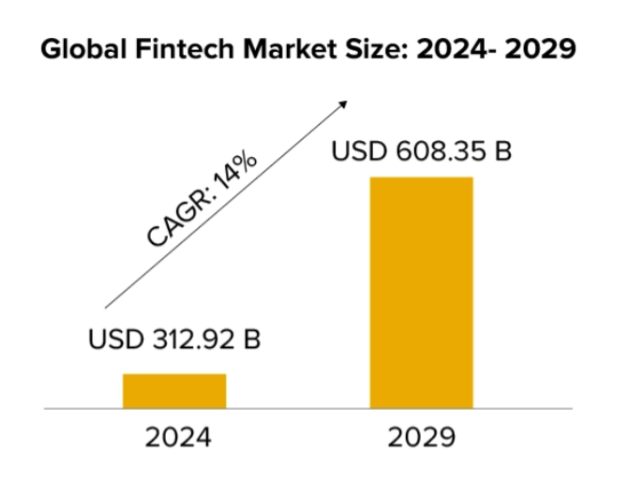

Fintech Market overview

The fintech industry is growing at a steady pace. According to data from Expert Market Research, the global fintech market is expected to reach around $324 billion by 2028, expanding at an annual growth rate of roughly 9.2%.

Insights from Statista suggest that digital payments will see massive user growth, with the total number of users likely to hit nearly 4.8 billion by 2028.

Reports from Exploding Topics indicate that the digital payments segment alone could surpass $10 trillion in global transaction value by 2027, driven largely by the rise of eCommerce and mobile-first users.

What are the different types of fintech apps and their cost?

Fintech is a broad space. Not every app is built the same way, and the cost can vary heavily depending on complexity, compliance, and scale.

A simple fintech app can start around ₹8–10 lakhs, while a full-scale, secure platform can go beyond ₹1–3 crores.

Here’s a breakdown that actually reflects real-world builds.

1. Digital Payment Apps (UPI, Wallets, P2P Transfers)

These are apps that allow users to send and receive money instantly.

Features

- UPI integration

- QR code payments

- Bank linking

- Transaction history

- Notifications

Cost Breakdown

Level | Cost (USD) | Cost (INR) |

Basic MVP | $10,000 – $18,000 | ₹8 – ₹15 Lakhs |

Mid-Level (secure + scalable) | $18,000 – $35,000 | ₹15 – ₹30 Lakhs |

Advanced (high traffic, enterprise) | $35,000 – $85,000 | ₹30 – ₹70 Lakhs |

What drives cost

- Payment gateway integration

- Real-time transaction handling

- Security and encryption layers

2. Digital Banking Apps (Neo Banks)

Why Businesses Prefer Bangalore for UX Expertise

These apps act like a full bank but operate digitally.

Features

- Account creation and KYC

- Balance and transaction tracking

- Debit card integration

- Spending insights

- Customer support

Cost Breakdown

Level | Cost (USD) | Cost (INR) |

MVP (limited features) | $30,000 – $60,000 | ₹25 – ₹50 Lakhs |

Full Product | $60,000 – $180,000 | ₹50 Lakhs – ₹1.5 Cr |

Enterprise Platform | $180,000 – $400,000+ | ₹1.5 – ₹3+ Cr |

What drives cost

- KYC verification systems

- Core banking integration

- Regulatory compliance (RBI, etc.)

- Backend architecture

3. Investment & Trading Apps

These apps allow users to invest in stocks, mutual funds, or crypto.

Features

- Real-time market data

- Portfolio tracking

- Buy/sell functionality

- Analytics and reports

- AI-based recommendations

Cost Breakdown

Level | Cost (USD) | Cost (INR) |

Basic Investment App | $25,000 – $50,000 | ₹20 – ₹40 Lakhs |

Advanced Trading App | $50,000 – $110,000 | ₹40 – ₹90 Lakhs |

Pro / High-Frequency System | $120,000 – $250,000+ | ₹1 – ₹2+ Cr |

What drives cost

- Real-time data APIs

- High-speed transactions

- Data visualization

- Risk and compliance systems

4. Lending & Loan Apps

Apps that provide personal loans, BNPL, or credit services.

Features

- User onboarding & KYC

- Credit scoring

- Loan application & approval

- EMI tracking

- Payment reminders

Cost Breakdown

Level | Cost (USD) | Cost (INR) |

Basic Lending App | $18,000 – $35,000 | ₹15 – ₹30 Lakhs |

AI-Based Credit System | $35,000 – $100,000 | ₹30 – ₹80 Lakhs |

Full Lending Platform | $100,000 – $250,000 | ₹80 Lakhs – ₹2 Cr |

What drives cost

- Credit scoring algorithms

- Risk assessment models

- Third-party integrations (CIBIL, APIs)

- Fraud detection

5. Personal Finance & Expense Tracking Apps

Apps that help users track and manage money.

Features

- Expense categorization

- Budget planning

- Insights and reports

- Bank syncing

- Alerts

Cost Breakdown

Level | Cost (USD) | Cost (INR) |

Basic App | $10,000 – $25,000 | ₹8 – ₹20 Lakhs |

AI-Driven Insights | $25,000 – $60,000 | ₹20 – ₹50 Lakhs |

Advanced Analytics Platform | $60,000 – $110,000 | ₹50 – ₹90 Lakhs |

What drives cost

- Data aggregation

- AI insights and predictions

- UI/UX complexity

6. Insurance (Insurtech) Apps

Apps that help users buy, manage, or claim insurance.

Features

- Policy comparison

- Purchase and renewal

- Claims processing

- Document upload

- Notifications

Cost Breakdown

Level | Cost (USD) | Cost (INR) |

Basic App | $18,000 – $40,000 | ₹15 – ₹35 Lakhs |

Mid-Level Platform | $40,000 – $100,000 | ₹35 – ₹80 Lakhs |

Advanced Ecosystem | $100,000 – $180,000 | ₹80 Lakhs – ₹1.5 Cr |

What drives cost

- Integration with insurers

- Document processing

- Claims automation

Why build a fintech app?

Financial services have quietly shifted from physical spaces to screens. People don’t want to stand in queues, wait for approvals, or deal with paperwork anymore. They expect everything from payments to investments to happen instantly, on their phone, without friction.

If you’re thinking about building one, it’s usually because you see a gap. Faster payments, easier lending, smarter investing, better financial control. And fintech gives you the chance to solve that at scale.

Key Reasons to Build a Fintech App

- Growing digital-first users

More people are managing money through apps than ever before, especially in markets like India where UPI and mobile banking are widely adopted. - High demand for convenience

Users prefer quick, seamless financial services over traditional banking processes. Speed and simplicity win. - Multiple revenue opportunities

You can monetize through transaction fees, subscriptions, commissions, lending interest, or premium features. - Access to a large, untapped market

Millions of users are still underserved by traditional financial systems, especially in Tier 2 and Tier 3 cities. - AI and technology make entry easier

Building and testing fintech ideas is faster now, which lowers the barrier to getting started. - Stronger user engagement and retention

Financial apps are used frequently, sometimes daily, which creates long-term user relationships. - Opportunity to build trust-driven brands

Fintech isn’t just about features. It’s about reliability. If done right, users stick with you for years.

Must-Have Features for a High-Performing Fintech App

A fintech app is judged by how reliably it handles money, protects user data, and performs under real-world pressure. Users expect every action to work without errors, delays, or confusion. Strong fundamentals matter more than flashy features.

Secure User Authentication

Access to financial data must be tightly controlled. Multi-factor authentication, biometric login, and device recognition add essential layers of protection. A simple username and password setup leaves too many vulnerabilities.

Real-Time Transaction Processing

Payments, transfers, and balance updates need to reflect instantly. Any lag or inconsistency can create uncertainty for users. Systems must be built to handle concurrent transactions without failure, even during peak usage.

Bank-Grade Security and Encryption

Sensitive financial and personal data must remain protected at all times. End-to-end encryption, secure API communication, and regular security testing help reduce the risk of breaches and fraud. Security should be embedded into the system, not added later.

User-Friendly Dashboard and Insights

Users should be able to understand their financial activity without effort. Clear transaction histories, categorized spending, and simple visual summaries make the app more useful in everyday use. Complexity often leads to drop-offs.

Seamless Payment Integration

Support for multiple payment methods is essential. UPI, cards, net banking, and wallets should work without friction. Failed or inconsistent payment flows directly impact user trust and retention.

Smart Notifications and Alerts

Users rely on timely updates to stay informed. Instant alerts for transactions, suspicious activity, or due payments provide transparency and an added sense of control. Poor notification systems can leave users unaware of critical events.

Scalable Backend Infrastructure

Growth should not break the system. Backend architecture must support increasing users, higher transaction volumes, and continuous uptime. Performance issues at scale can quickly damage credibility.

Compliance and Regulatory Readiness

Financial applications must align with regulatory requirements. KYC processes, data protection laws, and industry standards play a major role in whether an app can operate and expand. Ignoring compliance can lead to serious legal and operational setbacks.

Factors Affecting Fintech App Development Using AI

AI can speed up development, but it also introduces new dependencies and risks. In fintech, these factors directly influence how reliable and scalable the final product will be.

Data Quality and Availability

AI systems depend heavily on data. Financial applications require clean, structured, and relevant datasets such as transaction history, user behavior, and credit information. Incomplete or inconsistent data leads to inaccurate predictions, weak fraud detection, and unreliable insights.

Regulatory Compliance

Fintech operates in a tightly regulated environment. KYC requirements, data protection laws, and financial regulations must be followed at every stage. AI tools do not automatically align with these rules. Each workflow still needs validation to ensure it meets legal standards, especially in regions with strict compliance frameworks.

Security Requirements

Handling financial data demands strong security measures. AI can assist in generating code, but it does not guarantee secure architecture. Encryption protocols, secure data storage, and protection against fraud must be carefully designed and tested.

Integration Complexity

A fintech app connects with multiple external systems such as payment gateways, banking APIs, and identity verification services. AI can help with initial integration, but real-world scenarios involve failures, inconsistencies, and edge cases that require manual handling and experience.

Scalability and Performance

An app that works during testing may fail under real traffic. Systems need to support high volumes of transactions without slowing down or crashing. AI-generated setups often require restructuring to perform reliably at scale.

Customization and Business Logic

Fintech products are rarely built on standard templates. Each app requires specific workflows, risk models, and user journeys based on the business model. AI works well with patterns, but precise customization still needs human input and decision-making.

Can AI Really Build a Fintech App?

AI can assist in building a fintech app, but it cannot independently deliver a production-ready product.

It can generate UI designs, write portions of backend code, and speed up early development stages. These capabilities make it useful for prototyping and initial builds.

However, fintech applications involve real financial transactions, sensitive data, and strict compliance requirements. Errors in such systems carry serious consequences, including financial loss and legal risk.

AI lacks the contextual understanding needed for:

- Regulatory alignment

- Risk handling

- System architecture decisions

- Managing transaction failures

- Ensuring long-term scalability

Developers are essential because they design and control how the system behaves in real conditions. They ensure stability, handle unexpected scenarios, and maintain accountability when issues arise.

The most practical approach is a combination of both. AI accelerates development and reduces repetitive work, while developers ensure the product is secure, compliant, and reliable. The balance is what turns a basic app into a functional fintech platform.

Building Fintech Apps with Zethic

The gap between a working prototype and a reliable fintech product often comes down to execution. Zethic focuses on combining AI-driven development speed with strong engineering practices to deliver apps that perform in real conditions. Every stage, from integrations to backend architecture, is handled with attention to security, scalability, and compliance. The goal is not just to build features, but to create systems that can handle transactions, protect user data, and operate without failure as the product grows.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

1. Can AI alone build a fully functional fintech app in 2026?

AI can help create prototypes, basic features, and even parts of the backend. A production-ready fintech app still requires structured development, security architecture, and compliance checks. Financial systems need reliability and accountability that AI alone cannot ensure.

2. How much can AI actually reduce fintech app development cost?

AI can reduce initial development time and cost by 20 to 40 percent, especially during design and early coding stages. Savings usually apply to prototyping and basic feature development. Costs related to security, compliance, and scaling remain largely unchanged.

3. What are the biggest risks of building a fintech app using AI tools?

Common risks include weak security implementation, lack of compliance with financial regulations, unreliable transaction handling, and poor scalability. AI-generated code may work in testing but fail under real-world conditions.

4. Which fintech features benefit the most from AI integration?

AI is most effective in areas like fraud detection, credit scoring, customer support chatbots, and personalized financial insights. These features rely on data patterns, where AI performs well when trained on quality datasets.

5. Do fintech startups still need a development agency if they use AI?

Yes. AI can assist with development, but agencies handle system architecture, integrations, compliance, and long-term scalability. Most serious fintech startups combine AI tools with experienced development teams to reduce risk.

6. How long does it take to build a fintech app using AI and developers together?

A basic fintech app can take 3 to 6 months, while a more complex and scalable platform may take 6 to 12 months or more. AI can speed up early stages, but testing, security, and compliance processes still require time.