- 8 MIN READ

- Views: 264

Payment Gateway vs Payment Aggregator: What Every Founder Should Know

By Ram Nethaji

Founder

User Interface Design

Getting your payment infrastructure right from day one gives you faster go-to-market, lower per-transaction costs at scale, and a checkout experience your customers trust. Understanding the difference between a payment gateway and a payment aggregator is one of the most consequential early decisions a founder makes.

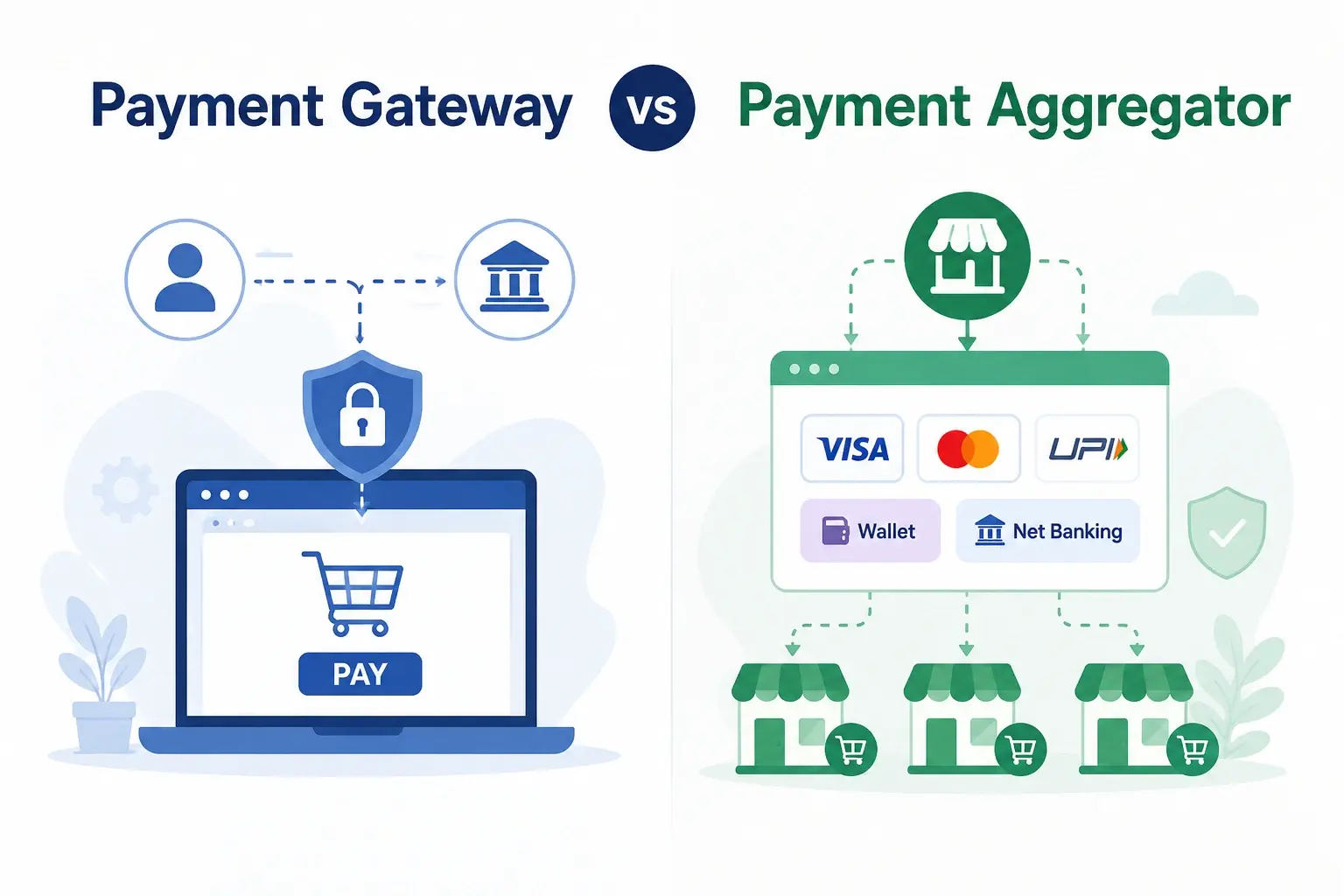

What Is a Payment Gateway?

A payment gateway is the technology layer that securely transmits payment data between your customer, your application, and the banking network. It encrypts card details, routes the transaction to the acquiring bank, and returns an approval or decline in real time. The gateway does not hold funds. It moves information.

In the most direct model, a business using a payment gateway obtains its own merchant account with an acquiring bank, which receives the settlement funds after each transaction. Setup typically takes one to three weeks and requires business documentation and bank approvals. It is worth noting that some gateway providers in India, such as CCAvenue, operate hybrid models that include acquiring relationships within the same platform, so the gateway-merchant account boundary is not always a hard separation.

Key characteristics:

- Each merchant has a dedicated merchant ID (MID) with the acquiring bank

- The business owns and manages PCI DSS compliance directly

- Per-transaction fees are lower at volume, typically 1.5% to 2% in India

- Full control over checkout experience, fraud rules, and settlement timing

Gateway reliability directly affects transaction success rates. Understanding payment failures in fintech applications is an important part of evaluating which infrastructure fits your product.

What Is a Payment Aggregator?

A payment aggregator is a platform that pools multiple merchants under a single master merchant account. Instead of each business holding its own relationship with an acquiring bank, the aggregator manages that relationship and sub-allocates payment processing to merchants beneath it.

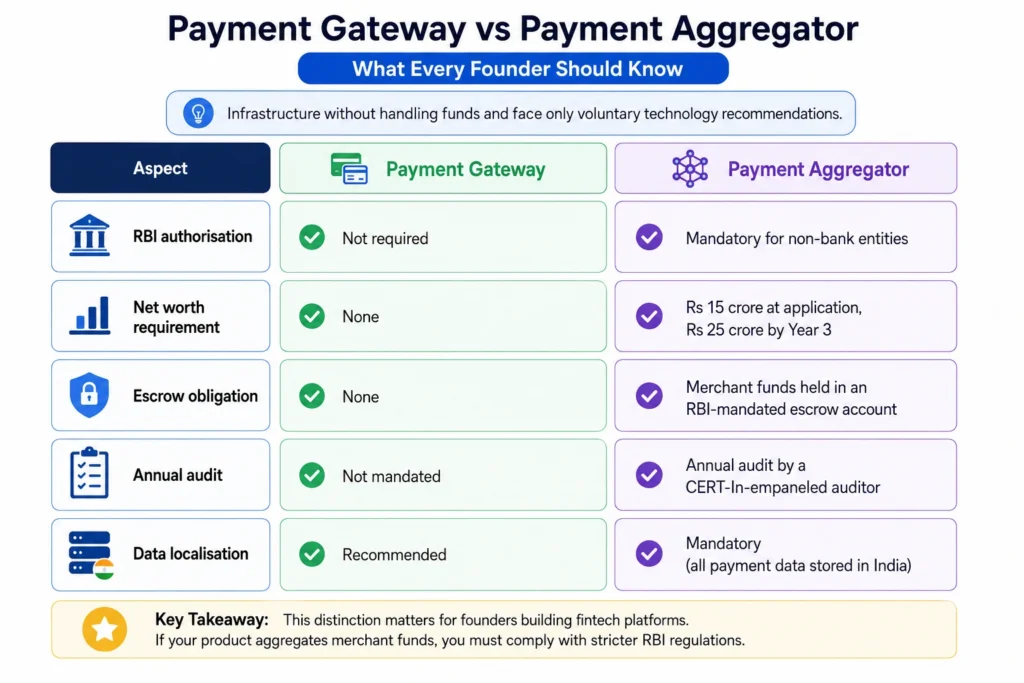

Stripe, Razorpay, PayU, and Cashfree are examples of payment aggregators. A business can integrate and go live within hours, without bank negotiations or lengthy approvals. In India, non-bank payment aggregators must obtain RBI authorisation under the Master Direction on Regulation of Payment Aggregators (2025) and maintain a minimum net worth of Rs 15 crore at application, rising to Rs 25 crore by the end of Year 3.

Key characteristics:

- No individual merchant account required

- Onboarding is typically completed in hours to days

- Per-transaction fees are higher at volume, typically 2% to 2.9%

- Aggregator manages compliance and fraud monitoring on your behalf

What Is the Real Difference Between a Payment Gateway and a Payment Aggregator?

The core distinction is control versus speed. Gateways give merchants direct ownership of the payment stack. Aggregators give merchants a shared stack with faster entry and less overhead.

| Parameter | Payment Gateway | Payment Aggregator |

|---|---|---|

| Merchant account | Dedicated, bank-issued | Shared under the aggregator’s master MID |

| Setup time | 1 to 3 weeks | Hours to days |

| Per-transaction fee (India) | 1.5% to 2% + GST | 2% to 2.9% + GST |

| Setup/annual fees | May apply | Typically zero |

| Compliance ownership | Merchant owns PCI DSS and sector-specific obligations fully | Aggregator manages PCI DSS; merchant retains data handling obligations under DPDP Act 2023 and sector-specific rules (NBFC, insurance) |

| Checkout customisation | Full control | Limited to the aggregator’s UI |

| Settlement timing | Negotiable with the bank | Set by aggregator (typically T+1 or T+2) |

| Chargeback handling | Merchant has direct standing with the acquiring bank | Governed by aggregator’s policies; the merchant has limited direct recourse |

| Fund-hold risk | Not applicable | Aggregator can withhold funds during fraud reviews or compliance audits |

How Do Payment Fees Actually Compare?

The per-transaction rate is not the full picture, and the headline rate varies significantly by payment method. Gateways may charge setup fees, annual maintenance charges, or integration costs that aggregators do not. Aggregators charge no upfront fees but take a higher cut per transaction, and rates are not flat across methods. UPI typically attracts zero MDR, domestic card transactions run at 2% to 2.5%, EMI transactions carry an additional processing fee, and international cards can reach 3% or higher depending on the aggregator and currency.

The breakeven point matters. At low volumes, an aggregator’s zero-setup model is cheaper in absolute terms, even at 2.5% per transaction. As monthly volume grows, the higher per-transaction rate compounds and a gateway’s lower rate begins to recover the fixed setup cost.

A practical reference point:

- At Rs 5 lakh/month volume, the difference between 2% and 2.5% is Rs 2,500/month

- At Rs 50 lakh/month, that same 0.5% gap equals Rs 25,000/month

- At Rs 1 crore/month, the gap reaches Rs 50,000/month, enough to justify gateway migration

UPI transactions in India carry zero MDR (Merchant Discount Rate) on standard bank-to-bank transfers regardless of which model you use, which meaningfully reduces blended cost for India-focused businesses. Per-transaction rates vary further by payment method cards, EMI, and international acquiring each carry different fee structures, detailed in Razorpay’s pricing breakdown. Gateway integration is also one input into hidden costs in fintech app development that includes compliance, maintenance, and engineering.

When Should You Use a Payment Aggregator?

A payment aggregator is the right starting point when speed and simplicity outweigh cost optimisation. For most pre-revenue and early-stage products, it is the correct default.

Use an aggregator when:

- You are pre-launch and need to accept payments within days, not weeks

- Your monthly transaction volume is below Rs 20 lakh, where the aggregator model delivers strong value relative to its fee structure

- You do not have the engineering bandwidth to manage PCI DSS compliance independently

- You are testing payment methods, markets, or pricing models before committing to infrastructure

When Should You Use a Payment Gateway?

A payment gateway becomes the right choice when payment volume justifies the setup overhead, or when your product requires control that aggregators cannot provide.

Use a gateway when:

- Monthly volume consistently exceeds Rs 25 to 50 lakh, and the per-transaction savings compound materially

- Your product requires a fully branded, custom checkout experience

- You operate in a regulated sector (lending, insurance, healthcare) with specific compliance or data isolation requirements

- You are building a marketplace or platform that itself needs to route payments to sub-merchants

For teams evaluating how much of the payment stack to build versus integrate, custom fintech app development covers the build vs. integrate decision in detail.

How Do Both Options Scale With Your Business?

Compliance requirements vary by market, but three frameworks affect most businesses processing digital payments.

| Business Stage | Monthly Volume | Recommended Option | Reason |

|---|---|---|---|

| Pre-launch / MVP | Below Rs 5 lakh | Aggregator | Zero setup, go live fast, test product-market fit |

| Early growth | Rs 5 to 25 lakh | Aggregator | The fee premium is still manageable, and compliance is handled |

| Scaling | Rs 25 to 50 lakh | Evaluate migration | Per-transaction savings compound, and gateway economics improve |

| Mature/enterprise | Above Rs 50 lakh | Gateway | Lower per-transaction rate, full control, branded UX |

Planning the gateway migration at the scaling stage means you execute it on your own timeline, with full engineering focus, rather than as a reactive project. Payment infrastructure decisions also compound with broader fintech app scalability challenges as transaction volume grows.

How Do Indian Regulations Treat Gateways and Aggregators Differently?

The RBI draws a clear regulatory line between the two. Under the Master Direction on Regulation of Payment Aggregators (September 15, 2025), payment aggregators are treated as entities that handle funds on behalf of merchants and are subject to mandatory RBI authorisation. Payment gateways, by contrast, are defined as entities that provide technology infrastructure without handling funds and face only voluntary technology recommendations.

This distinction matters for founders building fintech platforms. If your product aggregates payments from multiple merchants, you are likely operating as a payment aggregator under the RBI’s definition, not a gateway, and registration obligations apply from day one. A related operational requirement that affects both models is RBI’s Card-on-File Tokenisation (CoFT) mandate: since October 2022, no entity in the payment chain other than the card issuer or card network may store raw card data. Whether you use a gateway or aggregator, your product must work within a tokenised card flow for any saved-card or recurring payment feature.

What Should You Do Next?

For many founders, the decision between a gateway and an aggregator is clear in theory but harder to execute in practice. The real work in architecture is choosing the right payment methods, mapping compliance scope, and making sure the infrastructure you build at Rs 5 lakh/month still works at Rs 5 crore/month. Most of the decisions that shape that trajectory happen at the payment gateway software development stage, before the first integration is written.

That is the kind of decision that benefits from being made once, correctly, at the start. Teams that get it right typically have one thing in common: they thought through the payment stack as a product decision, not an integration task. Zethic builds exactly that, fintech products and payment-integrated platforms where the infrastructure is designed around the business model from day one.

About Zethic Technologies

Zethic Technologies is a trusted Web & Mobile App Development Company providing Custom Software Development Services to startups and growing businesses. We combine planning, development, and long-term thinking to deliver stable digital products.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

Can a business use both a payment gateway and a payment aggregator at the same time?

Yes. Some businesses use an aggregator for fast onboarding and domestic volume while integrating a gateway for specific use cases such as international payments, high-ticket transactions, or a custom-branded checkout. The two are not mutually exclusive.

Is Razorpay a payment gateway or a payment aggregator?

Razorpay functions as both. It provides aggregator services and also offers direct gateway integrations for larger merchants who want a dedicated merchant account. The product you use depends on your business size and agreement type.

Do I need RBI approval to use a payment aggregator in India?

No. A merchant using an aggregator does not need RBI approval. RBI authorisation applies to the aggregator itself, not to the merchants it serves. However, if you are building a platform that collects and settles payments on behalf of other merchants, your platform may itself qualify as a payment aggregator under the 2025 Master Direction and require authorisation.

What happens to my payments if a payment aggregator shuts down or loses its RBI authorisation?

If an aggregator loses authorisation, the RBI requires funds in the escrow account to be settled to merchants before operations cease. Under the 2025 Master Direction, aggregators must maintain merchant funds in a separate RBI-mandated escrow account with a scheduled commercial bank, which means your settled funds are ring-fenced from the aggregator’s own balance sheet. Funds already in transit at the time of shutdown may take longer to settle depending on the escrow terms.

Can a startup in India become a payment aggregator itself?

Yes, but the regulatory bar is high. Under the RBI’s 2025 Master Direction, a non-bank entity must be incorporated in India under the Companies Act 2013, obtain RBI authorisation through the Pravaah portal, and demonstrate a minimum net worth of Rs 15 crore at application, rising to Rs 25 crore by the end of the third financial year. Entities that aggregate payments on behalf of other merchants without this authorisation are operating outside the regulatory framework.