- 8 MIN READ

- Views: 1,895

How to Create a Payment Gateway in India: Steps & Compliance

By Ram Nethaji

Founder

Building a payment gateway in India involves RBI regulations, PCI-DSS compliance, banking partnerships, and real-time transaction systems. It’s the kind of infrastructure work that sits at the center of fintech application development in India.

UPI’s transaction volume keeps climbing month over month, and that scale is why businesses now weigh building their own gateway against a third-party provider, a call that depends on transaction volume, business model, and compliance capacity.

This guide covers how payment gateways work, the 2026 regulatory landscape, the build process, costs, and how to start a payment gateway company in India.

What Exactly Is a Payment Gateway?

A payment gateway is the layer between a merchant’s checkout and banking systems. It captures payment details, encrypts them, and routes the transaction for approval within seconds.

- Payment gateway: Captures and routes transaction data

- Payment processor: Handles backend communication between the gateway, the acquiring bank, and the issuing bank

- Payment aggregator: A licensed entity that collects and settles payments for multiple merchants

In India, building a gateway usually means building the full system: checkout, processing, and bank integrations. Businesses serving other merchants also need an RBI Payment Aggregator license, which is a core part of payment gateway software development at scale in India.

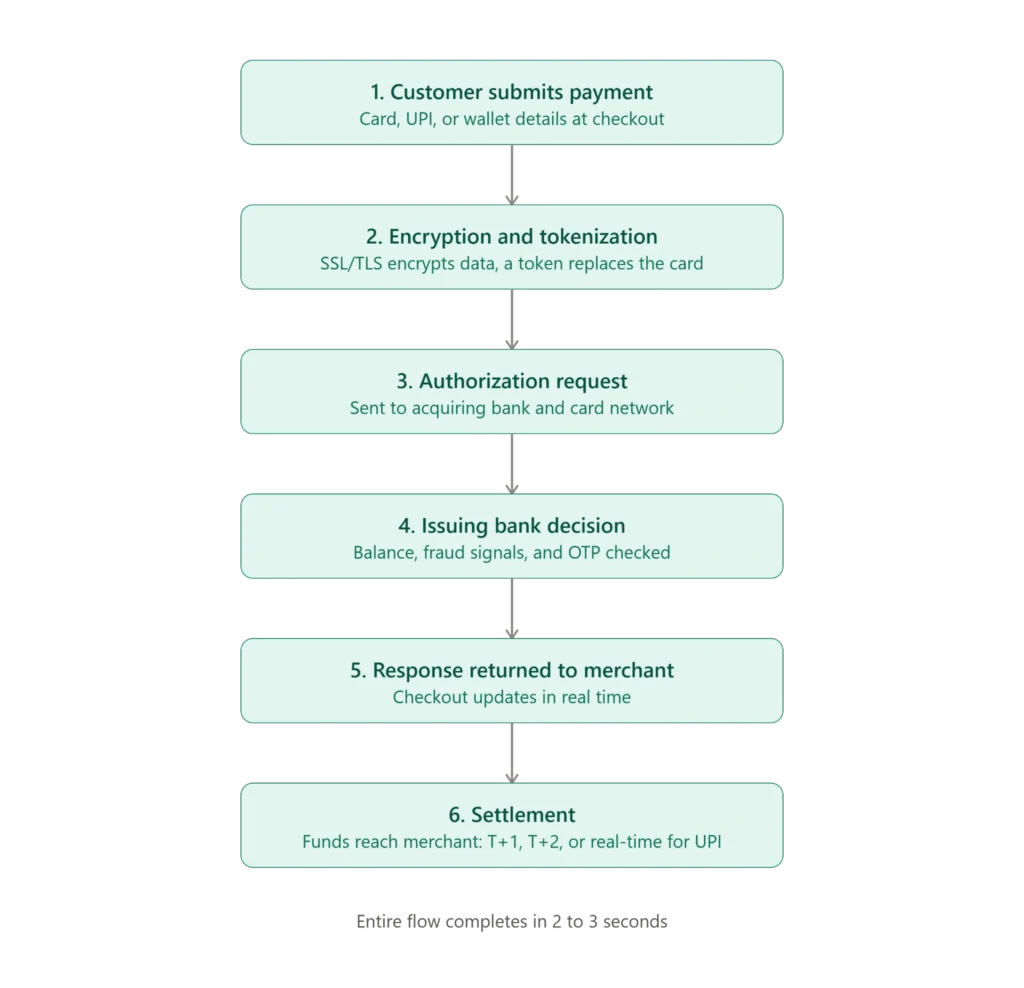

What Happens During a Payment Gateway Transaction?

A live transaction takes 2 to 3 seconds from “Pay Now” to confirmation:

- Card, UPI, or wallet details are submitted at checkout as a card-not-present (CNP) transaction

- Data is encrypted via SSL/TLS and tokenized, so no raw card data travels in plaintext

- The processor forwards the request to the acquiring bank and card network (Visa, MasterCard, RuPay)

- The issuing bank checks the balance, fraud signals, and 2FA (OTP), then returns approval or decline

- The gateway updates checkout in real time, and fulfillment proceeds

- Approved transactions settle on T+1, T+2, or real-time for UPI

RBI’s 2022 circular requires all entities, except card issuers and networks, to purge stored card data and transition to tokenization. It’s a compliance requirement, not a design choice.

Should You Build Your Own Payment Gateway?

Most businesses do not need to build one. Third-party solutions offer strong APIs and competitive pricing, and they already handle compliance.

Building makes sense when transaction volume is high enough that 1.5% to 3% fees add up, your model (marketplace, SaaS) requires collecting and settling payments for others, or you need custom flows and full control over payment data. Businesses serving other merchants also need an RBI Payment Aggregator license, a core part of building a custom payment gateway that operates at scale in India.

Think twice if RBI licensing (6 to 12 months, ₹15 crore net worth) and bank partnerships feel out of reach, or your team lacks payments expertise. Processing ₹10 crore monthly at 2% means ₹20 lakh in yearly fees, versus ₹1 to 2 crore to build; it comes down to long-term scale.

What Types of Payment Gateways Can You Build?

- Hosted gateway: Customers redirect to a third-party payment page; lowest compliance burden

- Self-hosted gateway: Checkout stays on the merchant’s server; more UX control, higher PCI-DSS scope

- API-hosted gateway: Fully custom checkout via APIs; requires full PCI-DSS Level 1 compliance

What Regulatory and Compliance Requirements Apply in India?

- PCI-DSS Level 1: Required for above 6 million annual transactions, with annual QSA audits

- KYC & AML: Merchant (and sometimes customer) verification plus ongoing transaction monitoring

- Data localization (RBI 2018): Indian payment data must stay on Indian servers; no foreign copies without RBI approval

- 2FA mandate: Every CNP transaction needs OTP-based authentication

- NPCI regulations: UPI support requires NPCI approval under its TPAP/PSP guidelines

- DPDP Act 2023: Explicit consent, purpose limitation, and breach notification for payment data

How Do You Build a Payment Gateway in India Step by Step?

What Technology Stack Do You Need to Build a Payment Gateway?

- Backend: Java Spring Boot, Node.js, or Go

- Frontend: React, Vue, React Native, or native iOS/Android

- Database: PostgreSQL, Redis

- Messaging: Kafka or AWS SQS for events and webhooks

- Infrastructure: AWS/GCP India regions, monitored via Datadog, ELK, or CloudWatch

How Much Does Payment Gateway Development Cost in India?

| Cost Category | INR (₹) | USD ($) |

|---|---|---|

| Core Development | ₹40L – ₹80L | $48,000 – $96,000 |

| PCI-DSS Certification | ₹8L – ₹20L | $9,600 – $24,000 |

| RBI Compliance | ₹5L – ₹10L | $6,000 – $12,000 |

| Bank Deposits | ₹20L – ₹50L | $24,000 – $60,000 |

| Infrastructure (Year 1) | ₹8L – ₹20L | $9,600 – $24,000 |

| Fraud Systems | ₹5L – ₹15L | $6,000 – $18,000 |

| Annual Maintenance | ₹10L – ₹15L | $12,000 – $18,000 |

A fully compliant gateway typically costs ₹1 crore to ₹2 crore ($120,000 to $240,000) in year one. Payment gateway development cost varies with payment rails, compliance scope, and domestic versus cross-border use. Building in phases, core features first, is the more practical path.

What Challenges Should You Plan for When Building a Payment Gateway?

So, Should You Build or Integrate a Payment Gateway?

For most businesses, integrating an established gateway is the faster, lower-risk path; building only makes sense at meaningful transaction volume with the license, capital, and team to support it. Companies that do build typically need support across architecture, license documentation, API development, and PCI-DSS readiness.

Zethic works with fintech teams on exactly this kind of payment infrastructure work in India, backed by a dedicated regulatory technology and unified banking solutions practice that covers everything from PA license documentation to production-grade transaction systems. Teams weighing this decision are welcome to talk to Zethic about their specific numbers.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

How do you start a payment gateway company in India?

How long does it take to get a Payment Aggregator license from the RBI?

Realistically, 6 to 12 months from application submission, since the RBI commonly sends queries requiring additional documentation for incomplete applications. There’s no guaranteed timeline, so fundraising and product plans should account for the full range.

What is the minimum capital required to build a payment gateway in India?

The RBI Payment Aggregator license requires a minimum net worth of ₹15 crore, scaling to ₹25 crore within three years. Beyond that, expect ₹1 to 2 crore in development costs and ₹20 to 50 lakh in banking security deposits, putting total capital outlay before going live at roughly ₹2 to 3 crore.

Can a startup without fintech experience get a PA license?

It’s possible, but the RBI scrutinizes the promoter’s background and the credibility of the business plan closely. Having a founding team member with financial services experience, or engaging a fintech compliance consultant, meaningfully strengthens the application.

How do you get a payment gateway for your website in India?

The fastest way is to integrate an established provider like Razorpay or PayU through their APIs, usually a few days of work with compliance already built in. Building from scratch only makes sense at meaningful transaction volume, with the licensing, capital, and team in place to support it.