- 8 MIN READ

- Views: 142

Open Banking vs Embedded Finance: What Founders Must Know

By Ram Nethaji

Founder

User Interface Design

Embedded finance transaction value in the US alone is projected to reach $7 trillion in 2026, accounting for 10% of all US financial transactions. The B2B embedded finance opportunity sits at $185 billion globally. UPI, India’s open API payment infrastructure, processed 228.3 billion transactions worth Rs 300 lakh crore in 2025, surpassing Visa in daily transaction volume. These are not future numbers. The infrastructure is already built. What separates the products that use it well from those that do not is understanding which model actually fits what you are building.

What Is the Difference Between Open Banking and Embedded Finance?

Open banking and embedded finance are often treated as synonyms. They are not. One is about data access. The other is about financial product delivery. The distinction matters at the architecture stage, not just the definition stage.

| Aspect | Open Banking | Embedded Finance |

|---|---|---|

| Core function | Regulated, consent-based sharing of financial data via APIs | Integration of financial products (payments, lending, cards, insurance) into non-financial platforms |

| What gets built | Budgeting tools, account aggregation, credit scoring, bank-to-bank payments | BNPL at checkout, in-app wallets, gig worker payouts, branded debit cards |

| Who controls data | Customer consents to share data with a third party | The platform owns the financial experience; the bank or BaaS provider sits in the background |

| Regulatory model | Highly regulated: PSD2 (EU), UK Open Banking Standard, CFPB Section 1033 (US), Account Aggregator framework (India) | Varies by product type; platforms partner with licensed institutions for compliance |

The two models are not competing. Open banking is often the data and connectivity layer that embedded finance products sit on top of.

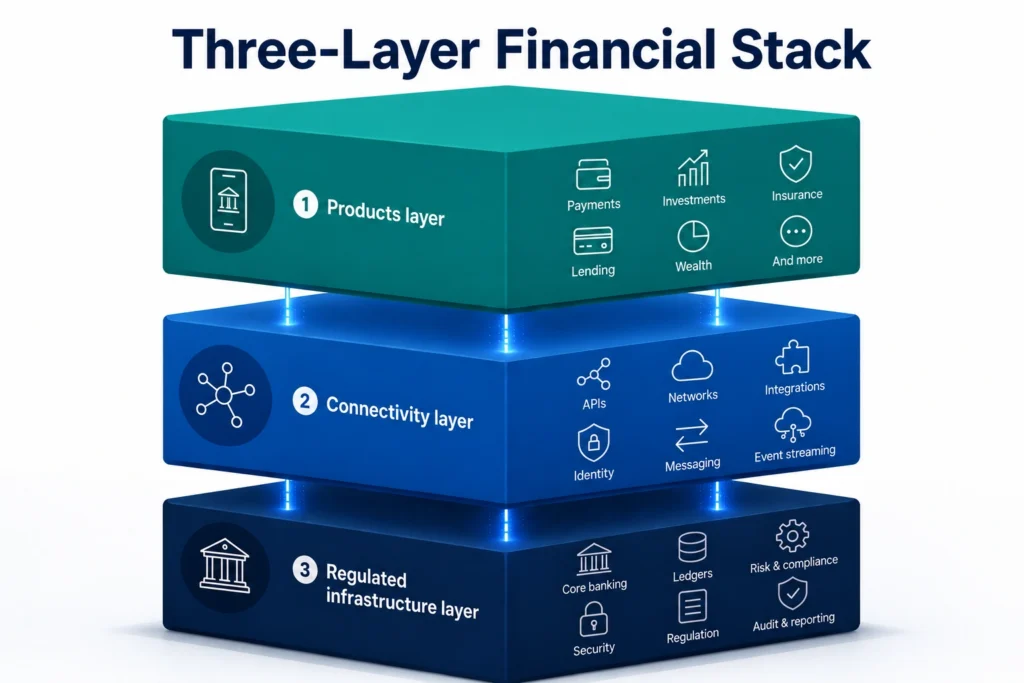

How Does the Three-Layer Financial Stack Work?

Understanding why open banking and embedded finance interact rather than compete requires seeing the full stack. In practice, three layers operate together.

- Products layer: The financial products users interact with: BNPL, in-app payments, lending, insurance, business accounts, and card issuing. These are built by non-banks on top of the layers below. Examples include Shopify Balance, Uber’s driver payouts, and Amazon Pay.

- Connectivity layer: API platforms that move financial data between source systems and the products above, with user consent. Plaid, TrueLayer, Codat, and India’s Account Aggregator-licensed entities sit here. This is where open banking standards operate.

- Regulated infrastructure layer: The rails on which money and data actually move: payment networks (UPI, SEPA, ACH, Faster Payments), sponsor banks that hold deposits and issue cards, card networks, and KYC data sources. No financial product works without this layer.

The regulated infrastructure layer is also where payment gateway software development services come into the picture. Acquirer routing, settlement logic, and payment rail selection all sit at this layer and cannot be changed cheaply once the product is live.

An embedded finance product picks the infrastructure it needs: open banking for account verification, UPI or ACH for payouts, and a sponsor bank for card issuing.

What Role Does BaaS Play Between Open Banking and Embedded Finance?

Banking-as-a-Service (BaaS) is the middle layer that makes embedded finance possible for non-banks. It is frequently confused with both open banking and embedded finance, but it is neither.

BaaS is a model where a licensed bank exposes its regulated functions (accounts, payments, cards, lending, and KYC) as APIs that non-bank businesses can integrate into their own products. The KYC in fintech layer is one of the most complex components to get right, since it sits at the intersection of identity verification and regulatory compliance across every product that uses BaaS.

How it connects to the other two models:

- Open banking: Provides the data access layer by reading account balances, verifying income, and initiating payments.

- BaaS: Provides the regulated infrastructure layer by issuing accounts, holding funds, and issuing cards under a banking licence.

- Embedded finance: Represents the product layer, delivering the user-facing experience built on top of BaaS infrastructure, sometimes using open banking data as an input.

In India, BaaS operates through licensed partner banks (such as RBL Bank, SBM Bank India, and Yes Bank) that expose their regulated functions through APIs under the RBI’s framework. The Account Aggregator network functions as India’s open banking connectivity layer within this stack.

Which Model Fits Your Product?

The right model depends on what your product does with money: whether it reads financial data, moves it, holds it, or lends it. Each use case maps to a different layer of the stack.

| Product Type | What You Need | Model |

|---|---|---|

| Personal finance / budgeting app | Read account data, categorise transactions | Open banking (connectivity layer) |

| Lending platform | Verify income, assess creditworthiness in real time | Open banking data + BaaS credit infrastructure |

| E-commerce platform | Accept payments, offer BNPL at checkout | Embedded finance (payments + lending via BaaS) |

| Neobank | Accounts, cards, transfers, savings | BaaS + embedded finance product layer |

| SaaS platform | Embedded invoicing, payouts to vendors or contractors | Embedded finance (BaaS-issued accounts + ACH/UPI rails) |

| Gig economy platform | Real-time worker payouts, earnings wallets | Embedded finance (BaaS payouts + open banking for account verification) |

Products that only need to read and analyze financial data sit in open banking. Products that need to hold, move, issue, or lend money sit in embedded finance, built on BaaS infrastructure. The product layer, what users see and interact with, is where the financial experience is won or lost. A fintech design agency that understands the compliance and data constraints of each layer is what separates financial products that feel native from those that feel bolted on. The neobank row in the table above is the clearest example of all three layers working together: neobank app development requires BaaS infrastructure for accounts and cards, open banking connectivity for data, and an embedded finance product layer that users actually interact with.

How Does Open Banking vs Embedded Finance Work in India?

India has its own version of each layer, and both are more advanced than most markets globally.

- Account Aggregator (AA) framework: India’s regulated equivalent of open banking. Licensed by the RBI, Account Aggregator entities act as consent managers. They do not store financial data; instead, they securely route it between Financial Information Providers (banks, insurers, mutual funds) and Financial Information Users (lending apps, wealth platforms) with explicit user consent. As of 2025, more than 100 million accounts are live on the AA network across major banks.

- UPI as embedded finance infrastructure: UPI is not just a payment method; it is an open, interoperable payment API that any licensed entity can build on. In 2025, UPI processed 228.3 billion transactions worth Rs 300 lakh crore, according to NPCI product statistics, surpassing Visa in daily transaction volume. Credit-on-UPI, launched in 2024 and expanding through 2025, enables banks and NBFCs to extend credit lines directly on the UPI rail, making UPI the world’s largest embedded lending distribution infrastructure.

- RBI’s open banking roadmap and the DPDP Act: These are the two primary regulatory anchors for fintech products in India. The RBI has signalled plans to expand open banking beyond the Account Aggregator framework to include insurance and pension data. The Digital Personal Data Protection (DPDP) Act, 2023 adds consent management and data minimization obligations on top of existing Account Aggregator and KYC requirements for any product processing Indian user data.

Can You Use Both Together?

Yes. The most defensible fintech products in 2025 and 2026 use open banking data to improve the embedded finance product sitting on top of it.

Three real-world patterns:

- BNPL with open banking underwriting: A BNPL provider at checkout uses open banking to check the customer’s live bank balance and transaction history before approving an instalment plan. The product is embedded finance, while the underwriting data comes from open banking.

- Neobank with AA-powered credit scoring: An Indian neobank uses the Account Aggregator (AA) network to pull a user’s financial data from multiple institutions, feeds it into a proprietary credit model, and extends a UPI credit line, all within the same app. This combines all three layers into a single user experience.

- SaaS platform with embedded payouts: A B2B SaaS platform embeds vendor payments and payroll through BaaS APIs. Open banking verifies vendor bank accounts before the first payout, while embedded finance powers the ongoing payment experience.

The products that use both technologies effectively understand where each layer begins and ends. That architectural clarity increasingly separates well-designed fintech applications from products that outgrow their infrastructure at the first major scaling event.

What Should You Do Next?

For most product teams, the architecture decision between open banking, embedded finance, and BaaS does not happen once: it evolves as the product adds features. A lending product that starts with open banking data for credit scoring eventually needs lending software development services to disburse loans, and the cost of adding each layer is one of the hidden costs in fintech app development that most initial product budgets do not account for.

That sequencing decision- which infrastructure to own, which to integrate, and how the layers connect- is where the real engineering and product work happens in fintech software development. Zethic builds fintech products and payment-integrated platforms where those decisions are made at the architecture stage, before the first integration is written.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

Is open banking the same as embedded finance?

What is BaaS, and how does it relate to open banking vs embedded finance?

BaaS (Banking-as-a-Service) is the regulated infrastructure layer that lets non-banks offer financial products. Open banking provides the data connectivity above it. Embedded finance is the product experience on top. BaaS is the middle layer that makes embedded finance possible without a banking licence.

Does India have open banking?

Yes. India’s Account Aggregator (AA) framework is the regulated equivalent of open banking. It lets users consent to share financial data across institutions via licensed AA entities. UPI functions as India’s embedded payment infrastructure: open, interoperable, and available to any licensed builder.

Which should a fintech startup build on first: open banking or embedded finance?

It depends on what the product does with money. If the product reads and analyses financial data (budgeting, credit scoring, account aggregation), start with open banking. If the product holds, moves, or lends money (payments, BNPL, neobank), start with embedded finance via a BaaS partner.

Can a non-bank offer financial products in India using embedded finance?

Yes, through a licensed BaaS partner bank or NBFC. Non-banks can embed payments via UPI, offer credit via credit-on-UPI with an NBFC partner, and manage accounts through a sponsor bank, all without holding a full banking licence. RBI’s regulatory framework governs each product type separately.