- 8 MIN READ

- Views: 32

Payment Gateway Security: How to Protect Every Digital Transaction

By Ram Nethaji

Founder

User Interface Design

Every time a customer enters their card details at checkout, that data travels through a chain of systems in under three seconds. Building the right layers from the start costs less than recovering from the breach that finds the gaps you left. Global card fraud losses reached $33.41 billion in 2024 (Nilson Report, 2026), and the average cost of a data breach hit $4.88 million the same year (IBM Cost of a Data Breach Report 2024. Payment gateway security is not a compliance checkbox. It is an architectural decision.

What Is Payment Gateway Security?

Payment gateway security is the set of protocols, technologies, and controls that protect financial data as it moves between a customer, a merchant, and the banking networks that authorize the transaction. It covers the full data lifecycle: capture, transmission, processing, and storage.

A secure gateway does four things simultaneously:

- Encrypts data so it cannot be read if intercepted

- Tokenizes card numbers so real credentials never sit on merchant systems

- Authenticates every party in the transaction chain

- Monitors transactions in real time to flag anomalies before they cause damage

Why Do Payment Gateways Get Breached?

Most breaches do not happen because attackers are sophisticated. They happen because businesses underestimate how many entry points their payment infrastructure exposes. A single misconfigured API or unpatched dependency is enough.

The most common attack vectors include:

- Man-in-the-middle (MITM) attacks: Data intercepted between the user’s browser and the gateway server

- SQL injection and XSS: Malicious scripts injected through payment forms to extract stored data

- Third-party script injection (Magecart): Malicious JavaScript embedded via compromised analytics, tag manager, or ad scripts on checkout pages to skim card data in real time, without touching your backend at all

- API vulnerabilities: Poorly secured endpoints that leak transaction details or allow unauthorized access

- Credential stuffing: Automated login attacks using stolen username and password combinations

- Insider threats: Employees with excessive system access are creating unmonitored exposure

Infrastructure gaps that lead to security breaches often overlap with those that cause payment failures in fintech applications, making architectural decisions doubly consequential.

What Does a Secure Payment Gateway Architecture Look Like?

| Layer | What It Contains | Key Security Controls |

|---|---|---|

| Public Layer | Customer-facing checkout, payment forms, APIs | TLS 1.2+, WAF, rate limiting, DDoS protection |

| Application Layer | Transaction logic, fraud detection, session management | OAuth 2.0, MFA, role-based access control (RBAC), input validation |

| Data Layer | Card data storage, logs, and settlement records | AES-256 encryption at rest, tokenization, strict access controls, audit logging |

Effective gateway design maintains clear separation between these three layers. No single breach should be able to cross all three. Isolated network zones reduce lateral movement and protect sensitive payment data even when the perimeter is compromised. Architecture decisions also directly affect real-time transaction infrastructure, where speed and security trade-offs are resolved at the design stage rather than after launch.

How Do You Secure a Payment Gateway End to End?

Securing a gateway requires decisions at the architecture stage, not just at deployment. Retrofitting security onto a live payment system is significantly more expensive and less effective than building it in from the start.

Key controls every gateway must have:

- TLS 1.2 or higher: On all data in transit, with certificate pinning on mobile clients to prevent interception even on compromised networks

- Tokenization: To replace card numbers with non-sensitive tokens that are useless outside your system; the actual PAN never touches your application server

- 3D Secure 2 (3DS2) authentication: For high-risk transactions, which passes device fingerprint and behavioral signals to the issuing bank for frictionless risk scoring rather than a blanket OTP step

- Fraud detection with machine learning: To score transactions in real time against velocity, geolocation, and behavioral baselines, flagging anomalies before authorization rather than after settlement

- Least-privilege access: Enforced at the infrastructure level; service accounts are scoped to specific operations, not broad database permissions, so a compromised microservice cannot read the full cardholder table

For businesses building custom payment gateway development, the decision between building in-house versus integrating a certified third-party gateway has a direct impact on PCI DSS scope. Integrating a hosted gateway substantially reduces the compliance surface your team must manage.

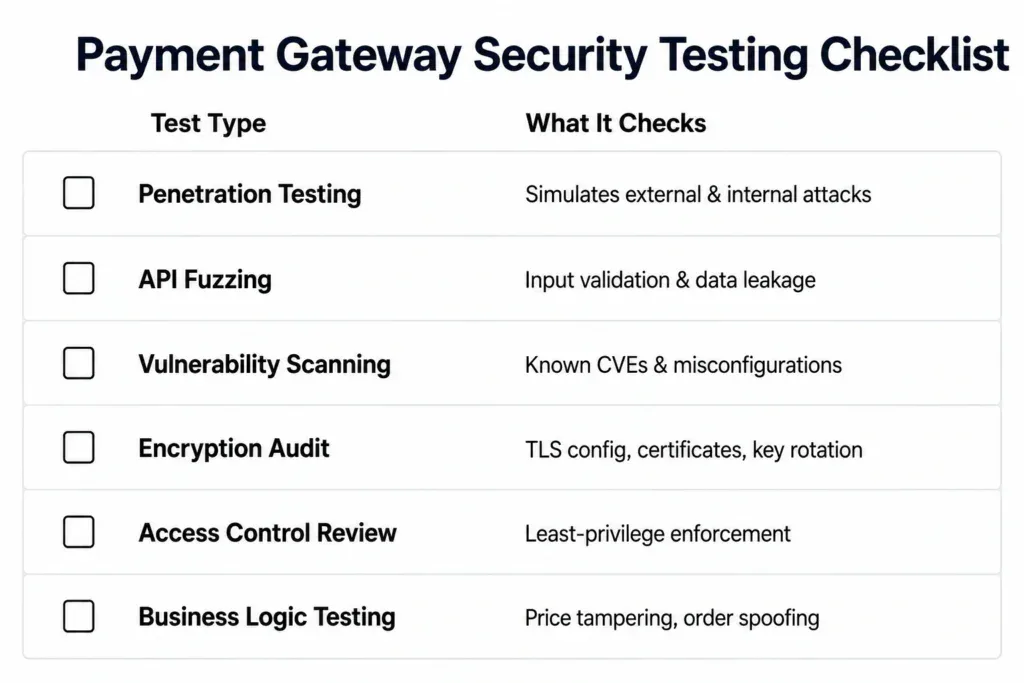

What Should a Payment Gateway Security Testing Checklist Include?

What are the key trade-offs in FinTech Startups?

Business logic testing is the most commonly skipped test category and the most consequential. Automated scanners cannot detect logic flaws because the application behaves correctly at a technical level; the flaw is in the business rules, not the code. A well-documented example: attackers have exploited negative quantity inputs in e-commerce checkout flows to reduce cart totals rather than increase them, generating fraudulent discounts that are invisible to WAFs and vulnerability scanners. According to HackerOne’s 8th Annual Hacker-Powered Security Report, business logic errors rank in the top 10 most reported vulnerability categories, with a roughly 5% year-over-year increase. These require manual review by engineers who understand the full transaction flow.

Which Compliance Standards Apply to Payment Gateway Security?

Compliance requirements vary by market, but three frameworks affect most businesses processing digital payments.

| Standard | Applies To | Core Requirements |

|---|---|---|

| PCI DSS v4.0 | Any business storing, processing, or transmitting card data globally | Encryption, tokenization, quarterly pen tests, access controls, audit logs |

| GDPR (EU) | Businesses processing payment data of EU residents | Data minimization, breach notification within 72 hours, right to erasure |

| RBI Guidelines (India) | Payment aggregators and gateways operating in India | Data localization, mandatory security audits, and RBI registration for payment aggregators |

For businesses operating in India, the RBI’s 2020 guidelines on payment aggregators added significant requirements around data storage and audit obligations. Non-compliance can result in revocation of operating authorization, not just fines. For the full technical requirements under PCI DSS v4.0, refer to the PCI DSS v4.0 resource hub.

Understanding which frameworks apply is the starting point. The harder question is how to build a product that satisfies all of them without rebuilding your security posture after every audit.

What Should You Do Next to Secure Your Payment Gateway?

For many businesses, the challenge is not understanding payment security but implementing it correctly while balancing compliance requirements, speed to market, and engineering capacity. Getting the architecture right from the first sprint means security controls, PCI DSS scope decisions, and fraud logic are built in rather than retrofitted.

Zethic works with fintech teams and product companies at exactly this stage, helping map the security stack before a line of code is written. If you are planning a fintech product, ecommerce platform, or any application that processes payments, explore Zethic’s fintech software development services or visit Zethic.

About Zethic Technologies

Zethic Technologies is a trusted Web & Mobile App Development Company providing Custom Software Development Services to startups and growing businesses. We combine planning, development, and long-term thinking to deliver stable digital products.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

Is PCI DSS compliance enough to secure a payment gateway?

No. PCI DSS sets a minimum security baseline, but compliance audits do not actively probe for logic flaws, API vulnerabilities, or real-time fraud patterns. Regular penetration testing and business logic reviews are required alongside compliance.

What is the difference between encryption and tokenization in payment security?

Encryption scrambles data so it cannot be read without a decryption key. Tokenization replaces sensitive data entirely with a non-sensitive substitute (a token) that has no value outside the system that issued it. Both are necessary; they protect data at different stages of the transaction.

How does the RBI's data localization rule affect payment gateway security in India?

RBI requires that payment data related to Indian transactions be stored only on systems located within India. This affects gateway architecture decisions, cloud provider selection, and backup strategies for businesses processing Indian card payments.

What is the difference between a hosted payment gateway and an integrated gateway from a security perspective?

A hosted gateway redirects customers to a third-party payment page, which means card data never passes through your servers, and your PCI DSS scope is significantly reduced. An integrated gateway keeps the customer on your site throughout checkout, which improves the experience but requires your team to implement and maintain the full security stack, encryption, tokenization, input validation, and access controls directly.

How do Magecart-style attacks work, and how can they be prevented?

RBI requires that payment data related to Indian transactions be stored only on systems located within India. This affects gateway architecture decisions, cloud provider selection, and backup strategies for businesses processing Indian card payments.

How often should a payment gateway security audit be conducted?

At minimum, a full security audit should run quarterly and after every significant infrastructure change, third-party integration, or major code release. PCI DSS v4.0 mandates quarterly vulnerability scans and annual penetration tests as a baseline, but businesses processing high transaction volumes or operating in regulated markets such as India should treat monthly automated scanning and bi-annual manual penetration testing as the practical standard.