- 8 MIN READ

- Views: 64

How to Build a KYC and AML Module for Fintech Apps

By Ram Nethaji

Founder

User Interface Design

Global AML, KYC, and sanctions penalties totalled $3.8 billion in 2025, down 18% year-on-year but still representing sustained enforcement pressure across every institution type. Digital asset firms and money transmitters accounted for the largest share of fines, with regulators consistently citing weak KYC in fintech onboarding as the root cause rather than transaction-layer failures. For any product that touches user identity or money movement, KYC in fintech is a product engineering decision with direct regulatory consequences.

What Is the Role of KYC in Fintech Apps?

KYC in fintech verifies a user’s identity at onboarding and assesses the risk they bring to the platform. AML monitors transactions across the user lifecycle to detect suspicious patterns. A well-built module treats both as one system with shared data, scoring, and audit trails.

The three core functions are:

- Identity verification: Confirming the user is real, present, and who they claim to be

- Risk assessment: Scoring the user based on profile, geography, behaviour, and external data

- Ongoing monitoring: Continuous screening for changes that move the user between risk tiers

Most major AML fines in 2025 traced back to inadequate identity verification at onboarding, not transaction-layer failures. Compliance architecture is now a core part of fintech app development, not a layer bolted on before launch.

What Are the Core Components of a KYC and AML Module?

Five components, treated as connected services that share a common risk engine:

- Identity verification: Document capture, OCR, face match, liveness detection

- AML screening: Checks against sanctions lists, PEP databases, and adverse media

- Risk scoring engine: Combines verification data, screening results, geography, and behavioural signals into one score per user

- Transaction monitoring: Real-time rule-based and ML-based detection, with thresholds tied to user risk score

- Case management and reporting: Audit logs, investigator workflow, and structured reporting to regulators such as the Financial Intelligence Unit India via FINnet 2.0

The risk score at onboarding must directly inform transaction monitoring thresholds. Otherwise, the module flags too much or too little, which is also where KYC architecture intersects with payment gateway software development, since fraud rules and transaction routing share the same risk signals.

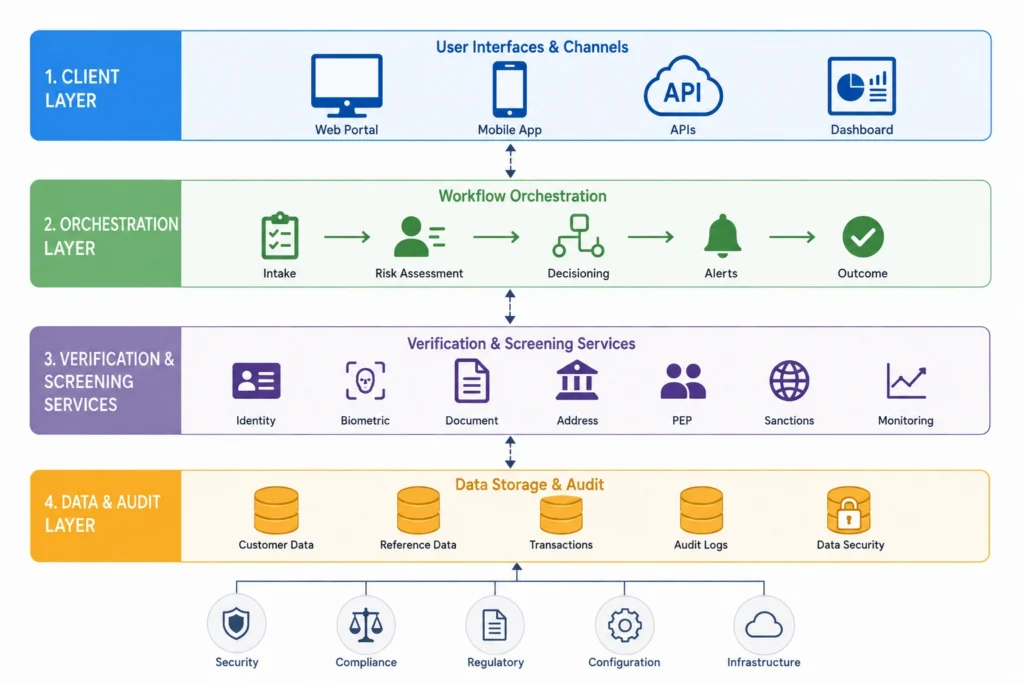

What Does a KYC and AML Module Architecture Look Like?

Four layers:

- Client layer: Mobile and web onboarding, document upload, biometric capture, status updates

- Orchestration layer: API gateway routing verification requests, managing session state and retries

- Verification and screening services: Independent microservices for document verification, face match, AML screening, and risk scoring

- Data and audit layer: Encrypted storage for documents, immutable audit logs, regulatory reporting pipelines

The orchestration layer is where a custom build earns its value. Vendors handle individual checks well; combining their outputs into one coherent decision is where the product differentiates. The KYC module also sits next to the payment stack; the same architectural discipline that underpins payment gateway security applies to how identity data flows through the verification layer.

What Should You Build vs Integrate in a KYC and AML Module?

| Component | Build or Integrate | Reason |

|---|---|---|

| Document verification (OCR, authenticity) | Integrate (Digio, Onfido, Sumsub, AuthBridge) | Vendor maintains templates across 200+ countries |

| Face match and liveness detection | Integrate | Specialist models; vendor handles deepfake updates |

| AML screening (sanctions, PEP, adverse media) | Integrate (ComplyAdvantage, Refinitiv, Dow Jones) | Watchlists update daily; data licensing is the cost |

| Aadhaar eKYC and DigiLocker (India) | Integrate via licensed KUA/AUA partner | UIDAI access requires direct licensing |

| Risk scoring engine | Build | Your scoring logic on your data is the differentiator |

| Transaction monitoring rules | Build base rules, integrate ML detection | Custom rules reflect your product’s risk profile |

| Case management workflow | Build | Investigator UX and escalation are operational IP |

| FIU-IND reporting (goAML) | Build the integration | Standardised format; one-time work |

The principle: integrate where data, certification, or scale are the value. Build where the logic and workflow are the product, the same boundary line that defines custom fintech app development across the rest of the product stack.

What Are the RBI KYC Rules for Fintech in India?

RBI replaced the 2016 KYC Master Direction with a new sector-specific framework on 28 November 2025, consolidating roughly 3,500 directions into 238 Master Directions across 10 institution types, including commercial banks, NBFCs, and payment banks.

Three rules carry the most engineering weight:

- V-CIP (Video-based CIP) is now standardised across institution types. Verification must happen in real time with both the agent and the customer visible. Sessions must be recorded and stored.

- Tiered KYC is mandatory. Low-risk users can be onboarded with lighter checks and lower transaction limits; higher tiers require full document verification. The architecture must support both from day one.

- Periodic re-verification intervals: 10 years for low-risk, 8 years for medium, 2 years for high. Most fintech products replace this with perpetual KYC.

PMLA (2002) remains the parent legislation. Records must be retained for at least five years, and suspicious transactions must be reported to FIU-IND. V-CIP, tiered KYC, and document upload flows all sit in front of the user, which is why onboarding UX in a regulated product is now a working concern for any fintech design agency and not just an engineering question.

How Do You Handle Perpetual KYC and Ongoing Monitoring?

Perpetual KYC replaces fixed re-verification intervals with continuous monitoring that triggers re-verification only when signals change.

Three patterns:

- Continuous screening against sanctions, PEP, and adverse media lists as those lists update

- Behavioural risk signals from transaction patterns, login geography, and device fingerprint feed the risk score in near real time

- Automatic re-verification triggers when the score crosses a threshold, documents expire, or adverse media hits appear

This satisfies the continuous monitoring expectation in the RBI 2025 framework and the FATF risk-based approach guidance that underpins it. Continuous compliance built into the product layer is now one of the defining requirements of regulated fintech software development.

How Much Does It Cost to Build a KYC and AML Module?

Engineering cost-only vendor API fees scale with verification volume separately.

| Scope | Cost (Rs) | Cost ($) | Timeline |

|---|---|---|---|

| Basic KYC (identity verification + AML screening, single jurisdiction) | Rs 15 to 30 lakh | $20,000 to $40,000 | 8 to 12 weeks |

| Full module (identity + AML + risk scoring + transaction monitoring) | Rs 35 to 70 lakh | $50,000 to $100,000 | 14 to 20 weeks |

| Enterprise (multi-jurisdiction, perpetual KYC, FIU reporting, case management) | Rs 70 lakh to 1.5 crore | $100,000 to $250,000+ | 22 to 36 weeks |

Vendor API fees run Rs 30 to Rs 100 per verification at low volumes, dropping to Rs 10 to Rs 30 at higher volumes. At 10,000 verifications per month, vendor fees can add Rs 3 to Rs 10 lakh monthly to operating costs. Vendor API spend is one line in a wider picture of hidden costs in fintech app development that most cost models miss until year two.

What Should You Do Next?

A KYC and AML module is one of the few parts of a fintech product where the cost of getting it wrong is much higher than the cost of building it well from the start. The components, data flows, and integration choices made at the architecture stage determine how the product handles its first audit, its first volume spike, and its first cross-border expansion.

Teams that get this right treat the KYC and AML module as a product decision with its own roadmap, not a compliance task to ship before launch. The vendor choices for document verification, the design of the risk scoring engine, and the way ongoing monitoring connects to transaction flows are all decisions worth making with the full context of where the product is going. That is the kind of fintech product engineering work Zethic is built around.

About Zethic Technologies

Zethic Technologies is a trusted Web & Mobile App Development Company providing Custom Software Development Services to startups and growing businesses. We combine planning, development, and long-term thinking to deliver stable digital products.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

What is the difference between KYC and AML in fintech?

KYC verifies who a customer is at onboarding. AML monitors what they do afterwards. KYC is one input into the broader AML programme.

How long does it take to build a KYC and AML module?

Basic verification: 8 to 12 weeks. Full module with risk scoring and transaction monitoring: 14 to 20 weeks. Enterprise builds with multi-jurisdiction support: 22 to 36 weeks.

Can a fintech in India use Aadhaar for KYC?

Yes, through a licensed KUA or AUA partnership. RBI has clarified that Aadhaar is not mandatory, so the module must support alternative documents alongside Aadhaar eKYC.

What happens if a fintech fails to comply with KYC in fintech regulations?

Should a fintech build custom or use an off-the-shelf platform?

A hybrid usually works best: integrate vendor APIs for document verification, AML screening, and biometrics, then build the risk scoring engine, transaction rules, and case management in-house.