- AI

Artificial Intelligence

Emerging Tech

- Products

AI, Marketing & Sales

Financial Services

Banking

Logistics & Mobility

- Services

Strategy & Innovation

Intelligent Engineering

Partner to Scale

Have a project in mind?

- Industries

FinTech & Banking

Logistics & Supply Chain

Practice spotlight

- ROI Calculator

- Company

- 8 MIN READ

- Views: 513

Neobank App Development: Features, Architecture & Cost

By Ram Nethaji

Founder

FinTech app development cost

User Interface Design

Custom software development

FinTech app development services

The global neobanking market reached $382.8 billion in 2025 and is projected to surpass $552 billion in 2026, growing at a CAGR of roughly 47% through 2032. Revolut, one of the most closely watched benchmarks in the space, posted £4.5 billion in revenue in 2025 with 68.3 million customers across 40 markets. What Revolut, Monzo, and N26 have in common is not just a mobile-first experience but an architecture built for scale from day one.

What Is a Neobank and How Is It Different from a Digital Bank?

A neobank is a financial institution that operates entirely through a digital platform with no physical branches. It delivers banking services, accounts, payments, cards, lending, and savings through a mobile app or web interface, typically built on cloud-native infrastructure and third-party banking APIs.

A neobank is built from scratch as a digital-first entity, often operating under a Banking-as-a-Service (BaaS) sponsor bank or its own banking licence, depending on the market. The infrastructure, compliance model, and product architecture are fundamentally different. The user experience is also a regulated surface in neobank onboarding flows, transaction screens, and error states all carry compliance implications, which is why working with a fintech design agency that understands both product and regulation matters more here than in standard consumer apps.

- No physical branch infrastructure, all operations, onboarding, and support run through the app

- API-first product design: core banking, KYC, card issuing, and payments are integrated as modular services

- The regulatory model is a founding decision the licensing path determines the entire compliance and architecture scope

This is why neobank builds tend to go to specialist teams rather than generalist app shops. Zethic’s fintech software development in Bangalore practice works through licensing model, architecture, and build-vs-integrate decisions before onboarding UI is even sketched, since retrofitting compliance after a launch is far more expensive than designing for it upfront.

What Features Does a Neobank App Need?

Feature scope is one of the biggest drivers of both development cost and time to market. The right starting point depends on your target segment, regulatory model, and monetisation strategy. Building every feature at launch typically extends timelines without proportional benefit to early user retention.

Minimum Viable Product (MVP) Tier

- Digital Onboarding & KYC: Fully paperless user sign-up coupled with automated identity verification.

- Savings & Current Accounts: Core digital account setup allowing users to hold and manage balances safely.

- Domestic Fund Transfers: Instant wire and bank-to-bank electronic fund processing.

Full-Featured Tier

- UPI & Wallet Integrations: Seamless integration with instant mobile payment systems and local digital wallets.

- Bill Payments: Automated and manual utility bill management, tracking, and settlement.

- Spending Analytics: Intelligent personal finance management tools that visually categorize user expenses.

Enterprise Tier

- Lending & Credit Scoring: Native consumer lines of credit, personal loans, and automated risk scoring algorithms, an area covered by our dedicated lending software development services.

- Investment & Wealth Tools: Direct integration with mutual funds, stock trading portals, or automated micro-investing features.

- Business Accounts: Enterprise-grade business banking suites that support multi-user role permissions and team management.

Most successful neobank launches start at the MVP tier with one or two differentiated features and expand the advantages of a neobank and layer in differentiated features as the user base grows. The architecture decision matters more than the feature list at launch, because the architecture determines how much it costs to add features later. The payments layer inside a neobank is its own product decision. Getting it right typically requires dedicated payment gateway software development services, since acquirer integrations, UPI routing, and settlement logic sit outside the core banking layer and need their own architecture.

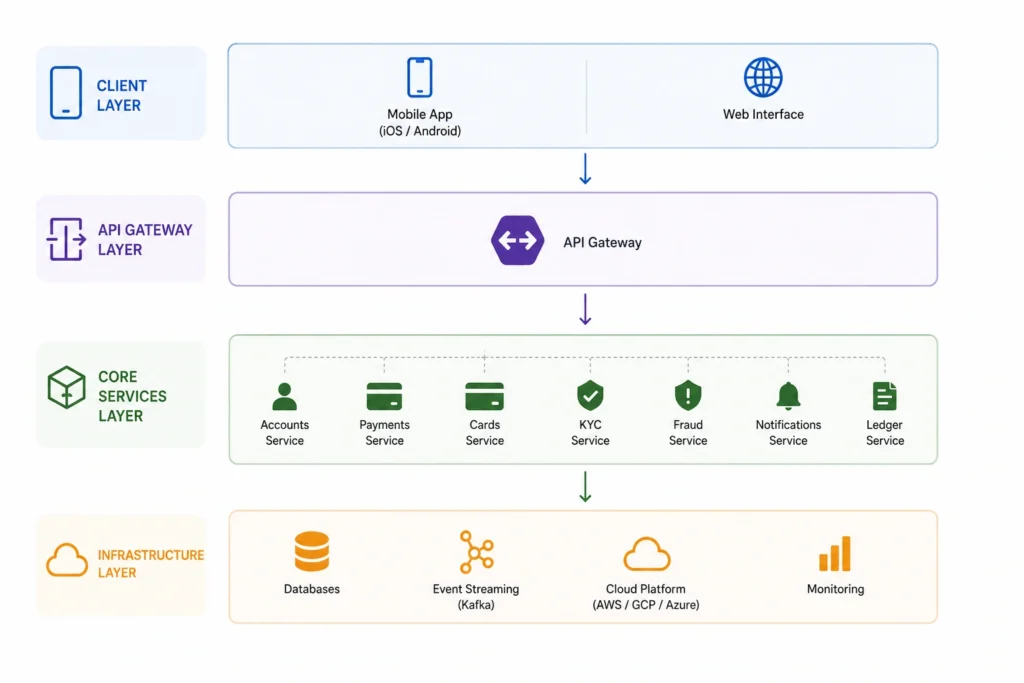

How Does Neobank App Development Architecture Work?

The architecture of a well-built neobank is layered, with each layer having a distinct responsibility. Trying to combine these layers, for example, building transaction logic into the frontend or coupling fraud rules to the core banking API, is the most common source of scalability issues as volume grows.

A production-grade neobank architecture covers four layers:

- Client layer: Mobile app and web interface, handling UX, authentication flows, and real-time notifications.

- API gateway layer: Routes all client requests, enforces authentication, manages rate limiting, and handles versioning across services.

- Core services layer: Microservices for accounts, payments, cards, KYC, fraud detection, notifications, and the transaction ledger, each independently deployable.

- Infrastructure layer: Cloud-native deployment, database management, event streaming (Apache Kafka for real-time transaction processing), and monitoring.

Each microservice in the core layer owns its own data store and communicates through event-driven messaging. This is what allows a neobank to scale individual components independently. The KYC service can be scaled during onboarding peaks without scaling the entire payments service alongside it.

What Should You Build vs Integrate in a Neobank?

The build vs integrate decision directly determines your development timeline, compliance scope, and long-term cost structure. Building every component in-house is rarely the right approach, and integrating everything limits what makes your product defensible.

- Core Banking Ledger: Integrate

Reason: Managing complex financial reconciliation logic requires extreme precision. Relying on specialist vendors ensures your core ledger is maintained full-time according to strict financial standards. - KYC and AML Verification: Integrate

Reason: Regulatory and compliance updates change frequently and are fully managed by the vendor. Trying to build an automated identity verification pipeline in-house adds roughly 6 to 12 months to your launch timeline. - Card Issuing: Integrate

Reason: Activating physical or virtual cards requires rigorous card scheme certifications. Integrating with established card processors lets the vendor handle complex card network rules and settlement logic. - Fraud Detection: Hybrid Approach

Reason: Utilising pre-trained models from specialised vendors saves months of initial development time. However, building your own proprietary logic on top of your live transaction data acts as a valuable long-term product differentiator. - Onboarding and Account UX: Build

Reason: The specific user journey, activation flow, and account dashboard layouts directly impact your user conversion rates. Creating a custom frontend makes your platform stand out and is a primary driver of customer retention. - Credit Scoring Model: Build

Reason: If consumer or business credit is your primary revenue engine, training a proprietary scoring model on your unique user data gives you a major competitive advantage. If lending is just a side feature, integrating with standard credit bureau data pulls is much more efficient. - Notifications and Messaging: Integrate

Reason: Sending text alerts or push notifications reliably at a massive scale is a solved technical problem. Building a messaging infrastructure from scratch is complex and does not offer a competitive advantage.

The principle is the same across every component: integrate where a reliable, auditable product already exists, and build where the logic is what differentiates your product from every other neobank using the same vendor. The same principle applies across the full product stack, where a custom fintech app earns its cost, precisely where off-the-shelf vendors stop being defensible.

What Licensing Model Do You Need to Launch a Neobank in India?

Licensing is the founding decision that determines your compliance architecture, partnership model, and regulatory obligations from day one. In India, three paths are viable depending on your product scope and capital position.

| Licensing Path | How It Works | Requirements | Best For |

|---|---|---|---|

| Full banking licence (Small Finance Bank or Payment Bank) | RBI-issued licence; operate as a licensed bank | Rs 200 crore paid-up capital (SFB); complex multi-year process | Large-scale, well-capitalised operators |

| BaaS via partner bank | Partner with a licensed bank; operate under their licence via API | Technology and compliance agreement with the partner bank | Fastest route to market; suitable for most funded startups |

| NBFC route | Obtain an NBFC licence from the RBI; offer lending and savings products without full banking | Rs 10 crore net owned funds; RBI registration | Fintech products focused on credit, lending, or BNPL |

Most neobank startups in India launch via the BaaS route, partnering with banks like RBL, Yes Bank, or SBM to access account issuance, payment rails, and card issuing under the bank’s regulatory umbrella. The NBFC route is chosen when lending is the primary product and the full banking licence is not required at launch.

How Much Does Neobank App Development Cost?

Development cost varies significantly by scope, team location, and compliance requirements. The figures below use India-based development rates for the Rs column and blended global rates for the $ column. These figures cover development only and do not include banking licence fees, BaaS partner costs, or ongoing compliance expenses.

| Scope | Development Cost (Rs) | Development Cost ($) | Timeline |

|---|---|---|---|

| MVP (onboarding, accounts, transfers, debit card) | Rs 40 to 80 lakh | $50,000 to $120,000 | 16 to 24 weeks |

| Full-featured (multi-method payments, analytics, support, wallets) | Rs 80 lakh to 1.5 crore | $120,000 to $250,000 | 24 to 40 weeks |

| Enterprise (lending, investments, business accounts, open banking) | Rs 1.5 to 3 crore | $250,000 to $500,000+ | 40 to 60 weeks |

Neobanks sit at the higher end of the mobile app development cost spectrum in India because compliance requirements, security audits, and third-party API integrations add substantial scope beyond standard feature development. A production-grade neobank in India should budget an additional Rs 30 to 60 lakh per year for cloud infrastructure, third-party API fees, and regulatory compliance costs that sit outside the development quote and compound quietly across years two and three, a pattern mapped in detail in the breakdown of hidden costs in fintech app development.

What Should You Do Next?

Building a neobank is less about having the right feature list and more about making the right architecture, licensing, and build-vs-integrate decisions at the start. Those decisions compound the right ones, making every subsequent sprint faster and cheaper; the wrong ones surface during compliance audits, scaling events, or licensing transitions.

Zethic builds fintech products and mobile applications where these decisions are made at the architecture stage, before the first line of code is written. The work spans onboarding flows, payment integrations, core banking API layers, and the compliance infrastructure that fintech software development needs from day one. If you are at the planning or scoping stage for a neobank or digital banking product, Zethic is a good place to start.

About Zethic Technologies

Zethic Technologies is a trusted Web & Mobile App Development Company providing Custom Software Development Services to startups and growing businesses. We combine planning, development, and long-term thinking to deliver stable digital products.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

What is the typical timeline for neobank app development?

Sometimes. If the POC was built on clean, scalable architecture, it can seed the MVP, but most POCs are quick experiments and should be treated as throwaway code.

How is neobank app development different from standard app development?

A neobank requires regulatory compliance from day one: KYC, AML, PCI DSS, and RBI guidelines in India alongside real-time transaction processing, multi-party API integrations, and a core banking ledger. Standard app development involves none of these constraints, which is why fintech-specific engineering experience matters at the architecture stage.

Can you launch neobank app development as a startup without your own banking licence in India?

Yes. The BaaS route allows a startup to launch under a licensed partner bank’s regulatory umbrella. This is the most common path for funded neobank startups in India and significantly reduces the capital and time requirements of the full banking licence process.

What are the most important architectural decisions in neobank app development?

Microservices vs monolith, event-driven vs request-driven transaction processing, and the choice of core banking provider are the three decisions with the highest long-term cost implications. Getting these right at the design stage determines how much it costs to scale, add features, and pass compliance audits.

How do you choose between a custom build and a white-label platform for a neobank?

White-label platforms reduce time to market and compliance scope at the cost of customisation and higher per-transaction fees at scale. Custom neobank app development gives full ownership of the product experience, data, and unit economics. The decision depends on your transaction volume trajectory, product differentiation requirements, and engineering capacity.