- AI

Artificial Intelligence

Emerging Tech

- Products

AI, Marketing & Sales

Financial Services

Banking

Logistics & Mobility

- Services

Strategy & Innovation

Intelligent Engineering

Partner to Scale

Have a project in mind?

- Industries

FinTech & Banking

Logistics & Supply Chain

Practice spotlight

- ROI Calculator

- Company

- 8 MIN READ

- Views: 147

What Does Banking Compliance Software Really Cost Compared to Non-Compliance?

By Ram Nethaji

Founder

FinTech app development cost

User Interface Design

Custom software development

FinTech app development services

Banks are spending more on compliance technology than at any point in the past decade. Yet regulators still handed out billions of dollars in fines last year alone. The real question for any bank evaluating a purchase is not whether to invest, but whether the software actually closes the gaps that cause these fines.

What Is Banking Compliance Software?

Banking compliance software is a system that tracks a bank’s regulatory obligations, checks transactions and processes against those rules, and generates the reports regulators require. It connects to core banking systems, customer databases, and transaction records to flag activity that falls outside approved limits.

Building this kind of system overlaps closely with custom fintech software development, since compliance modules typically sit alongside payment processing and account infrastructure rather than standing on their own. This is why banks often coordinate compliance builds directly with their payment gateway software development services provider, so transaction monitoring rules and payment routing logic are designed against the same data rather than reconciled after the fact. Most platforms also keep a record of every check performed, so a bank can show what it did and when if a regulator asks.

In practice, this covers checks like transaction limits, sanctions and watchlist screening, and reporting deadlines tied to specific regulators. A bank launching a new product, such as instant payments or digital lending, typically needs its compliance software updated at the same time the product goes live, not months afterward.

How Much Does Non-Compliance Actually Cost a Bank?

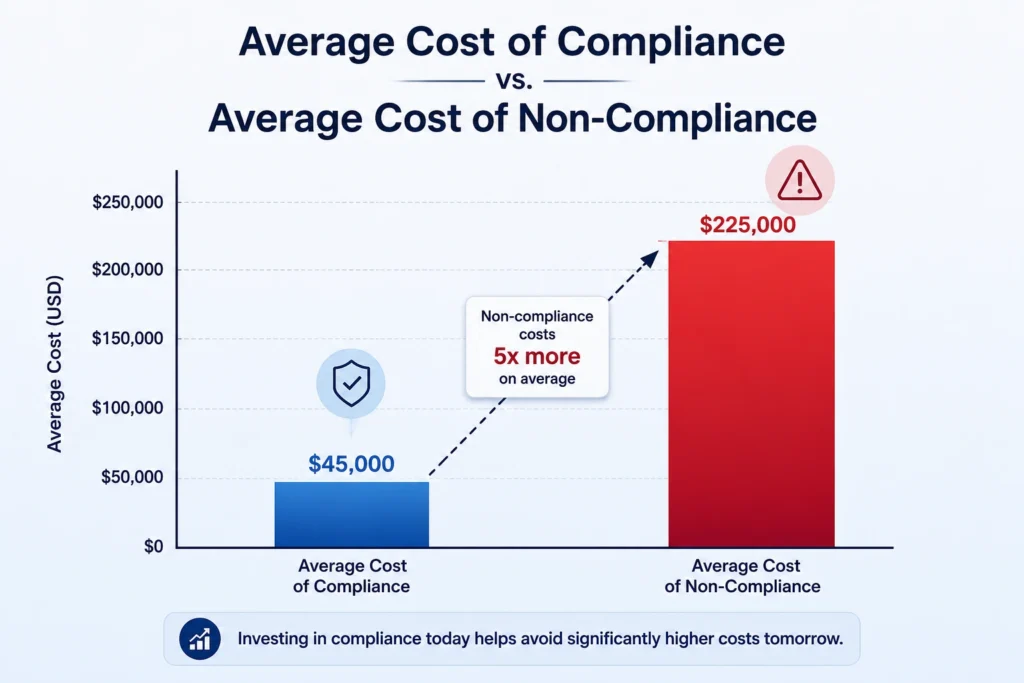

The gap between the cost of staying compliant and the cost of failing to comply is large and well documented. This gap becomes more visible once a bank quantifies both the fines regulators impose and the internal disruption that follows.

- The average annual cost of non-compliance across organizations is $14.82 million, compared to $5.47 million for maintaining compliance (Ponemon Institute and Globalscape, 2017)

- In October 2024, the U.S. Treasury’s Financial Crimes Enforcement Network assessed a $1.3 billion penalty against TD Bank for Bank Secrecy Act violations, the largest civil penalty ever imposed on a depository institution in FinCEN history (FinCEN, 2024)

- TD Bank was also required to accept a four-year independent monitorship to oversee remediation of its anti-money laundering program (FinCEN, 2024)

Remediation after a major compliance failure usually involves more than paying the fine itself. Banks often bring in outside consultants, retrain compliance staff, and rebuild transaction monitoring systems that should have caught the problem earlier. Much of this work traces back to compliance software that was never updated to match current regulatory requirements.

These figures point to a pattern: the fine itself is rarely the highest cost. Remediation, monitorships, and lost business tend to add up to far more than the original penalty.

What Does the RBI Require Indian Banks to Build for Compliance?

- On January 31, 2024, the Reserve Bank of India issued a directive on the internal compliance monitoring function, instructing regulated entities to move away from manual and spreadsheet-based compliance tracking. The circular requires banks, NBFCs, and other regulated entities to adopt integrated, workflow-based systems for internal compliance monitoring.

- Scheduled commercial banks, small finance banks, and payments banks fall under the directive.

- Regulated entities must review existing compliance tracking processes and update or replace them.

- Systems must support clear task assignment, escalation, and reporting across departments.

- Indian banks must also account for the Digital Personal Data Protection Act alongside the RBI requirements.

The circular does not name a single vendor or platform. Regulated entities can choose their own systems as long as the platform supports task assignment, audit trails, and reporting across departments. Smaller NBFCs are held to the same expectations as large commercial banks, even though their compliance teams are usually much smaller.

For banks operating in India, this means compliance software is no longer optional. It is a direct regulatory expectation with a defined scope.

Should a Bank Build or Buy Compliance Software?

There is no single right answer here. The decision depends on how specific a bank’s compliance needs are and how much internal engineering capacity it has. Regulatory complexity, existing core banking systems, and how quickly the bank needs to be compliant all factor into the choice as well.

| Factor | Build | Buy |

|---|---|---|

| Upfront cost | Higher requires a dedicated engineering team | Lower, subscription, or license-based |

| Timeline | 9 to 18 months for a working system | 2 to 6 months to first deployment |

| Control | Full control over logic and integrations | Limited to the vendor’s configuration options |

| Maintenance | Ongoing internal responsibility | Vendor handles regulatory updates |

| Best fit | Large banks with unique core systems | Mid-size banks and NBFCs with standard needs |

A hybrid path is common too: buying a base banking solutions platform and commissioning custom integration work for a bank’s specific core banking system, rather than choosing one extreme or the other.

Team size is often the deciding factor in practice. A bank that builds in-house usually needs a dedicated group of engineers and compliance analysts to maintain the system for as long as it stays in use, while buying shifts most of that ongoing maintenance to the vendor. Banks with smaller technology teams tend to lean toward buying for this reason alone. How Long Does It Take to Implement Compliance Software?

Implementation timelines vary by scope, but most projects follow the same sequence.

- Requirements and vendor selection, typically 4 to 6 weeks

- Integration with core banking and data systems, typically 6 to 10 weeks

- Testing against real compliance scenarios, typically 4 to 8 weeks

- Staff training and phased rollout, typically 3 to 6 weeks

A mid-size bank can expect a working system in roughly 4 to 6 months, a pace not unlike building a payment gateway in India, where legal review and testing often run in parallel. Larger institutions with multiple legacy systems often take longer, mainly due to integration work rather than the software itself.

Timelines stretch further when a bank operates across multiple states or countries, since each jurisdiction can add its own reporting formats and review cycles. Banks that skip the testing phase to save time often end up doing that work later anyway, once regulators or auditors flag gaps the software should have caught.

What Does It Actually Take to Close These Compliance Gaps?

The throughline across cost, regulation, and timeline comes down to the same point: compliance software only prevents fines when it stays current with both the rules and the bank’s own systems. That alignment matters more than whether the software was built in-house, bought outright, or stitched together as a hybrid.

This is the kind of work Zethic’s fintech software development in Bangalore team takes on directly with banking and NBFC teams, whether a project starts as a full build or as integration work layered onto a purchased platform. That includes RBI-aligned workflow systems, AML and KYC modules built around fraud detection and transaction security, and reporting tools matched to a bank’s specific regulatory scope- the same gaps this article has walked through from cost to implementation.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

Does every bank need compliance software, or only large institutions?

An MVP with core routing logic typically takes a few months. Full production systems with multiple integrations and real-time re-routing take longer.

How much does banking compliance software typically cost?

Costs vary widely by scope and deployment model, though broader research on the cost of non-compliance shows subscription-based platforms generally cost less upfront than a fully custom build.

Can existing core banking systems integrate with new compliance software?

Most modern compliance platforms are designed to connect with core banking, transaction, and customer data systems, though the integration effort depends on how old the existing systems are.

What happens if a bank misses the RBI compliance technology deadline?

Regulated entities that fail to update their systems risk regulatory scrutiny and potential penalties tied to inadequate compliance monitoring.

How often does compliance software need to be updated for new regulations?

Rule sets should update as soon as a regulator issues a change, since a system running on outdated rules still leaves a bank exposed even if the software itself works fine.