- 8 MIN READ

- Views: 246

White-Label vs Custom Payment Gateway: Cost-Benefit Breakdown

By Ram Nethaji

Founder

User Interface Design

Payment infrastructure is one of the few technical decisions that directly affect both your revenue and your compliance posture. For enterprise teams evaluating the build-versus-buy question, the real choice is rarely as binary as it appears. White-label gateway, custom-built gateway, or a hybrid of both, each option carries a fundamentally different cost structure, risk profile, and long-term ceiling.

What Is a White-Label Payment Gateway?

A white-label payment gateway is a fully built, PCI DSS-certified payment processing platform developed by a third-party provider and licensed to businesses to operate under their own brand. The provider manages the underlying infrastructure, compliance certifications, and core feature set, while the business customises the UI, branding, and checkout experience on top. Unlike a standard aggregator, the merchant owns the customer-facing brand and the payment relationship; the underlying technology stack is simply licensed rather than built, which is why white-label gateways are increasingly the starting point for fintech products that need a branded payments experience without an eighteen-month build timeline.

White-label gateways are offered as SaaS or licensed software. Setup typically takes two to four weeks. The business does not own the underlying technology but does own the merchant relationship and the branded experience delivered to customers.

Key characteristics:

- Deployment in two to four weeks versus twelve to eighteen months for a custom build

- PCI DSS Level 1 certification managed by the vendor, not the business

- Per-transaction fees typically 1.5% to 2% for low volumes, with volume discounts at scale

- Customisation limited to UI, branding, checkout flow, and routing rules within the vendor’s framework

What Is a Custom-Built Payment Gateway?

A custom-built payment gateway is proprietary infrastructure developed and owned entirely by the business. Every component, transaction routing, fraud detection, settlement logic, merchant dashboard, and compliance architecture is built, maintained, and operated in-house or by a dedicated development partner.

Shopify is the most cited real-world case. Shopify Payments, built as proprietary infrastructure, processed $61 billion in gross payment volume in Q4 2024 alone, and Merchant Solutions, which includes Shopify Payments, grew 35% year-over-year to become Shopify’s largest single revenue driver. The economics of owning the stack at that volume are self-evident. At that scale, every component such as API architecture, compliance layers, acquirer integrations, and fraud logic is built around the business’s specific transaction patterns rather than a vendor’s generalised framework, which is the core argument for building a custom payment gateway once volume justifies the investment.

Key characteristics:

- Full ownership of transaction data, routing logic, fraud rules, and settlement timing

- PCI DSS compliance is the business’s full responsibility, including annual audits

- Per-transaction costs drop significantly below 0.5% at high volumes

- Timeline of fourteen to forty weeks, depending on scope; enterprise multi-market builds at the longer end

What Does Each Option Actually Cost?

Build costs vary significantly by scope. The figures below use India-based development rates for the Rs column and blended global rates for the $ column.

| Scope Tier | Custom Build (Rs) | Custom Build ($) | White-Label Setup | White-Label Annual |

|---|---|---|---|---|

| MVP (card payments, basic fraud, dashboard) | Rs 25 to 40 lakh | $30,000 to $80,000 | Rs 0 to 5 lakh | Rs 8 to 15 lakh (fees + transaction cut) |

| Full-featured (multi-method, wallets, EMI, UPI) | Rs 40 to 80 lakh | $80,000 to $200,000 | Rs 2 to 8 lakh | Rs 15 to 30 lakh |

| Enterprise multi-market (cross-border, multi-currency, acquirer routing) | Rs 1 to 2 crore | $250,000 to $500,000+ | Rs 5 to 15 lakh | Rs 30 lakh+ |

White-label setup cost is low to zero, with ongoing fees that scale predictably with volume. The custom build cost is higher upfront. The per-transaction economics strengthen significantly as volume grows. Scope, compliance tier, and acquirer relationships each add layers to the final number. A full breakdown of what drives payment gateway development cost across these variables is worth mapping before committing to either model.

What Is the 3-Year Total Cost of Ownership?

| Cost Component | White-Label (3 Years) | Custom Build (3 Years) |

|---|---|---|

| Upfront build / setup | Rs 0 to 15 lakh | Rs 40 lakh to 2 crore |

| Annual maintenance | Included in fees | Rs 8 to 12 lakh/year (20% of build cost) |

| PCI DSS compliance | Vendor-managed | Rs 15 to 30 lakh/year (audit + team) |

| Engineering headcount | Minimal (integration only) | 3 to 6 dedicated engineers |

| Per-transaction cost at Rs 50 lakh/month | Rs 75,000 to 1.45 lakh/month | Rs 10,000 to 25,000/month at owned rates |

| 3-year total (mid-volume estimate) | Rs 75 lakh to 1.5 crore | Rs 1.5 to 3 crore |

The crossover point where custom-built TCO drops below white-label TCO is typically around Rs 50 to 75 lakh in monthly transaction volume for India-focused businesses, and approximately $10 million in annual transaction volume for global operations. What shifts that crossover point earlier or later is rarely the build cost itself; it is the compliance, maintenance, and third-party dependencies that make up the hidden costs of fintech app development and sit outside most initial estimates.

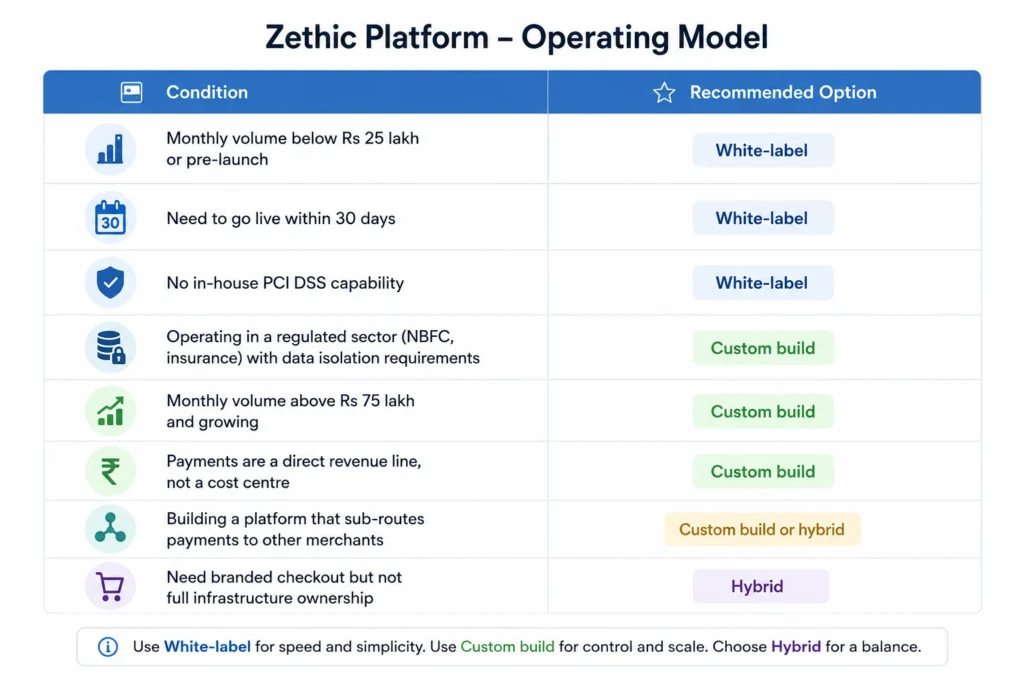

What Are the Build vs Buy Decision Triggers?

Neither option is universally correct. The right choice depends on your transaction volume, compliance obligations, engineering capacity, and how central payments are to your core product.

Is There a Hybrid Option?

Yes, and it is how many enterprise teams resolve the false binary. A hybrid model uses a white-label gateway as the certified processing core while building a custom layer on top for fraud logic, routing rules, checkout UX, and data pipelines. The business gets PCI DSS compliance without owning the certification and retains control over the logic that directly affects conversion rates and fraud outcomes.

The hybrid model works well when:

- Your product requires a fully branded, custom checkout experience, but you cannot justify an eighteen-month build timeline

- You need proprietary fraud models trained on your own transaction data without building the full payment stack

- You are in a regulated sector that requires data isolation, but your volume does not yet justify a full custom build

The key consideration with the hybrid model is that the vendor’s core architecture defines the boundaries of what can be customised. Logic at the acquirer routing layer, for example, may sit outside the vendor’s customisation framework, and that boundary is exactly where the build vs integrate decision in custom fintech app development becomes consequential, so validating it early is part of the vendor evaluation process.

What Happens to Vendor Lock-In Over Time?

Vendor lock-in with a white-label gateway is not just a Year 1 concern; it compounds. At Year 1, lock-in is manageable. Setup costs are sunk, integration is fresh, and the vendor’s pricing is typically competitive because they want retention. At Year 3, the dynamics shift. Your transaction data, merchant relationships, and checkout flows are embedded in the vendor’s infrastructure. Migration to a custom build or a different white-label provider requires rebuilding integrations, re-onboarding merchants, and absorbing a disruption window that most businesses cannot afford during a growth phase.

The practical implication: negotiate data portability, API access rights, and migration assistance into the contract before you sign, not when you decide to leave. Vendors who resist these clauses are signalling their lock-in strategy clearly. The migration, regulatory authorisation, acquiring bank relationships, and compliance architecture are what make creating a payment gateway in India a materially different undertaking from a standard software build, and worth understanding before the contract conversation begins.

What Should You Do Next?

For many enterprise teams, the real challenge is not choosing between white-label and custom; it is knowing when the economics, compliance obligations, and product requirements all point in the same direction at the same time. That inflexion point looks different for every business, and getting the architecture right at that moment is what determines whether payments become a cost centre or a competitive advantage. That is precisely the kind of problem dedicated payment gateway software development services are designed to solve, and what Zethic builds around.

About Zethic Technologies

Zethic Technologies is a trusted Web & Mobile App Development Company providing Custom Software Development Services to startups and growing businesses. We combine planning, development, and long-term thinking to deliver stable digital products.

Let Zethic help you build smarter Not just faster

Frequently Asked Questions

At what transaction volume does a custom gateway become more cost-effective than white-label?

For India-focused businesses, the practical crossover is around Rs 50 to 75 lakh in monthly volume, where per-transaction savings typically offset the annualised build and maintenance cost within twelve to eighteen months. For global operations, the commonly cited threshold is approximately $10 million in annual transaction volume.

Can a white-label gateway satisfy RBI compliance requirements in India?

Yes, provided the vendor holds RBI authorisation as a payment aggregator or has a licensed acquiring partner in India. Merchants inherit the vendor’s PCI DSS coverage, but data localisation obligations under RBI’s 2025 Master Direction still apply to the data infrastructure regardless of which model you use.

What is the most important ongoing cost to budget for in a custom gateway build?

PCI DSS compliance. Level 1 QSA audits run $50,000 to $150,000 per year globally and Rs 15 to 30 lakh per year in India. Building this into Year 1 alongside development cost avoids it becoming an unplanned expense in Year 2.

How long does it take to migrate from a white-label gateway to a custom-built one?

A well-planned migration typically takes eight to sixteen weeks, covering acquirer onboarding, API rebuilds, PCI DSS scoping, and merchant re-integration. The timeline extends when data portability was not negotiated into the original white-label contract, which is why that clause matters at the vendor selection stage.

Does a custom-built gateway require a separate RBI licence in India?

It depends on what the gateway does. If it only routes and processes payments without holding merchant funds, it operates as a technology layer and does not require standalone RBI authorisation. If it aggregates payments on behalf of merchants, it falls under the RBI’s 2025 Master Direction for payment aggregators and requires mandatory authorisation.

What engineering team size is needed to build and maintain a custom payment gateway?

A production-grade custom gateway typically requires three to six engineers across backend, security, and DevOps at the build stage, and two to four for ongoing maintenance. Compliance functions, PCI DSS evidence gathering, audit preparation, and vulnerability management are either handled by a dedicated security engineer or outsourced to a QSA firm.